Personal Finance for Students: How to Budget, Save Money, Build Credit, and Manage Expenses in 2026

By a 19-year-old creator, learning in public | For educational purposes only — not professional financial advice

🌍 Global Context Note: Banking products, loan terms, credit scores, taxes, and financial regulations vary by country. This guide includes examples from India and the US, but always verify local rules and rates before acting on anything here.

Nobody taught me this stuff.

Not at school. Not at home. Not anywhere.

I sat through years of lessons — history, science, math, English. But nobody ever explained how a bank account actually works. Nobody told me what happens when you ignore your spending. Nobody mentioned that the habits you build at 18 quietly shape the next twenty years of your life.

And then suddenly I had some money — a small allowance, a little from part-time work — and it disappeared. Every month. Without explanation.

I’d open my bank app and just stare at the number. Where did it go?

That confusion is what eventually pushed me to start learning about personal finance. And the first thing I realized? Almost nobody teaches this to students. Many students receive little or no formal personal finance education before graduating high school, according to research from the National Endowment for Financial Education (NEFE). That means most of us are figuring this out alone, usually after making a few expensive mistakes first.

This personal finance for students guide is my attempt to put everything I’ve learned in one place. Plain English. No confusing terms. No lectures. Just the real basics — explained the way I wish someone had explained them to me.

⚠️ Quick heads-up: I’m a 19-year-old writing this based on research and personal learning. Nothing here is professional financial advice. For important money decisions, please speak with a certified financial advisor or your bank directly.

🚀 New Here? Start With These Three Things Right Now

Before you read anything else, do these. They take under ten minutes total.

- Open your bank app and look at your last 30 days of transactions. Not what you think you spent — what you actually spent.

- Count every active subscription on your phone. Write down the monthly cost of each one.

- Pick one small, fixed amount — ₹200, ₹500, whatever won’t hurt — and commit to moving it to savings the moment money arrives next month.

That’s your starting point. Everything else in this guide builds from there.

Table of Contents

- What Is Personal Finance, Really?

- Terms That Confused Me (And What They Actually Mean)

- How to Track Your Expenses as a Student

- How to Budget When You’re a Student

- Setting Financial Goals That Actually Make Sense

- How to Save Money as a Student on a Low Income

- Banking Basics Every Student Should Know

- Student Loans: What You Should Know Before You Borrow

- How to Build Credit as a Student Responsibly

- Common Personal Finance Mistakes Students Should Avoid

- Disclaimer

- FAQ

- Final Thoughts + What To Do This Week

What Is Personal Finance, Really?

It sounds like a corporate term. It isn’t.

Personal finance just means how you manage your own money. That’s the whole thing. How much comes in. How much goes out. What you keep. What you owe. How you think about the future.

Nobody is born understanding this. It’s a skill. And like any skill, you get better by actually doing it — not by reading about it endlessly.

Here’s why it matters especially for students.

Right now, most of us don’t earn a lot. But we also don’t have a lot of obligations. No mortgage. No family to feed. No massive fixed bills. That combination — low income, low obligations — is actually a really useful window.

It’s the easiest time to build good habits from scratch.

Because here’s what I’ve learned: money habits stick. The ones you build at 18 or 19 tend to follow you. They either quietly work for you over time, or quietly work against you. And most people don’t realize which one is happening until years later.

I’m not saying this to scare you. I’m saying it because starting early — even with very little — genuinely matters.

You don’t need to be rich to start. You just need to pay attention.

Terms That Confused Me (And What They Actually Mean)

I want to be honest about something.

The first time I started reading about personal finance, I got confused and nervous almost immediately. Words like “CIBIL score,” “credit utilization,” “fixed deposit,” “SIP,” “compound interest” — they all sounded important. But nobody explained them in plain English.

I’d read one sentence and hit three unfamiliar terms. I’d Google one term and find two more I didn’t understand. It was exhausting.

So before we get into the actual guide, here are the terms that kept tripping me up — explained the way I wish someone had explained them when I first started.

Personal Finance Just how you manage your own money. Income, spending, saving, borrowing. That’s it. Nothing mysterious.

Budget A plan for where your money goes each month. Not a restriction — a decision. You decide in advance instead of wondering afterward.

Emergency Fund Money you keep set aside specifically for unexpected things. Broken phone. Sudden medical expense. A job gap. You don’t touch it for anything else. It’s your financial safety net.

Savings Account A basic bank account where your money earns a small amount of interest (usually 2.5–4% per year in India, though rates vary by bank and can change). Easy to access anytime.

Fixed Deposit (FD) You lock a sum of money with a bank for a fixed period — say, 6 months or 1 year. In return, the bank pays you a higher interest rate than a regular savings account (rates vary depending on the bank and deposit period). The catch: you can’t easily take the money out early without a penalty.

Compound Interest Interest on your interest. When you save money, you earn interest. Then next month, you earn interest on the original amount plus the interest from last month. Over years, this grows your money faster than simple interest. It’s one of the most important concepts in personal finance.

Credit Score A number that tells banks how trustworthy you are as a borrower. In India, it’s called a CIBIL score (300–900). In the US, it’s a FICO score (300–850). Higher is better. It affects whether you can get loans, credit cards, or even rent an apartment.

Credit Utilization The percentage of your credit limit you’re currently using. If your credit card limit is ₹20,000 and you’ve spent ₹6,000, your utilization is 30%. Many financial educators recommend keeping this below 30%, though lower is generally better.

SIP (Systematic Investment Plan) A way of investing a fixed small amount — say ₹500 — every month into a mutual fund, automatically. You don’t need to time the market. You just set it and let it run. Popular in India as a beginner investing method.

Mutual Fund A pool of money from many investors, managed by a professional. Instead of buying one stock, your money is spread across many — which reduces risk. Index funds are a common low-cost type.

Hard Inquiry When a bank or lender checks your credit history because you applied for a card or loan. Too many of these in a short time can slightly lower your credit score.

Moratorium Period For education loans in India — the gap between taking the loan and when repayments start. Usually 6–12 months after graduating or 1 year after getting a job, depending on the bank.

UPI (Unified Payments Interface) India’s digital payment system. When you pay someone using PhonePe, Google Pay, or Paytm — that’s UPI. Instant, free, and works 24/7.

Once I actually understood these terms, everything else made more sense. The guide below uses all of them — but now you already know what they mean.

How to Track Your Expenses as a Student

Before budgets, before savings, before any plan at all — you need to know where your money is actually going.

Most students have no idea. I didn’t.

I thought I was spending reasonably. Then I actually tracked one month. Food delivery I’d forgotten about. Subscriptions I hadn’t used in three weeks. Small random purchases that each felt harmless but together added up to a number I wasn’t proud of.

Tracking doesn’t fix anything on its own. But it makes everything visible. And you genuinely cannot manage what you cannot see.

I’ve been using the Expense Manager app by Bishinews to track my spending, and it’s been surprisingly helpful. It’s free, easy to use, and makes it simple to see exactly where my money goes each month. If you’re just getting started with budgeting, it’s a great option because you can log expenses quickly without dealing with complicated features.

Note: This is a personal recommendation based on my experience. I’m not affiliated with or sponsored by the developer.

Here’s How to Start

Step 1 — Pick a method you’ll actually use.

No fancy app required. A notebook works. A Google Sheet works. If you want an app, Walnut is decent for India. Your own bank’s statement page works fine too. Whatever you’ll actually open every day — use that.

Step 2 — Record every purchase for 30 days.

Every coffee. Every ride. Every time you tap your card or use UPI. No skipping, no rounding, no “I’ll add it later.” Just record it honestly.

Step 3 — Sort it into categories.

At the end of the month, group everything:

| Category | Examples |

|---|---|

| Essentials | Food, rent, transport, phone recharge |

| Education | Books, stationery, course fees, printing |

| Lifestyle | Eating out, movies, clothes, online shopping |

| Subscriptions | Netflix, Spotify, apps, cloud storage |

| Savings | Amount you actually moved aside |

| Random / Other | One-off purchases, unexpected costs |

Step 4 — Look at the totals honestly.

Where did most of your money go? What surprised you? No judgment here. Just awareness.

Step 5 — Make one small change next month.

Not ten. One. Cancel one unused subscription. Cook at home twice a week instead of ordering. Swap one expensive habit for a cheaper one. Small, sustainable shifts.

A Sample Monthly Student Budget (Example Only)

This is a rough example for a student in an Indian city with ₹10,000/month. Your numbers will be different — this is just to show what tracking might look like:

| Category | Example Amount | % of Income |

|---|---|---|

| Food & Groceries | ₹3,000 | 30% |

| Transport | ₹800 | 8% |

| Phone / Internet | ₹500 | 5% |

| Education Costs | ₹600 | 6% |

| Subscriptions | ₹500 | 5% |

| Eating Out / Fun | ₹1,600 | 16% |

| Savings | ₹2,000 | 20% |

| Random / Buffer | ₹1,000 | 10% |

| Total | ₹10,000 | 100% |

This is a hypothetical example. Costs vary significantly by city, lifestyle, and personal situation.

Five minutes a day. That’s all tracking takes. But most people never do it — and then wonder why they’re always running out of money before the month ends.

How to Budget When You’re a Student

Budgeting sounds like punishment. I know.

Like you’re going to be miserable, saying no to everything fun, staring at spreadsheets on a Friday night.

It’s not like that. A budget is just a plan. You’re deciding in advance where your money goes instead of being confused about it afterward. That’s it.

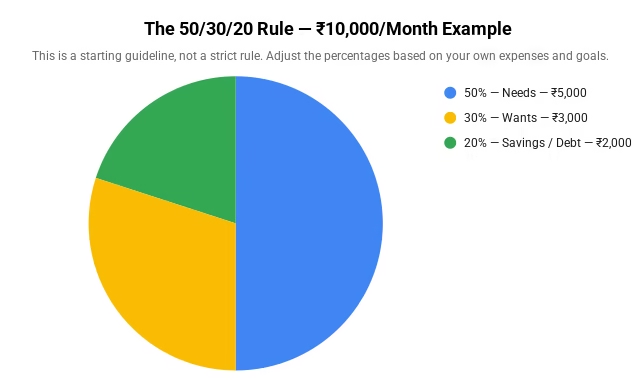

The 50/30/20 Method

This is the most beginner-friendly starting point I’ve found. Flexible, simple, and easy to remember.

Take your monthly income and split it roughly like this:

| Bucket | Percentage | What Goes Here |

|---|---|---|

| Needs | 50% | Rent, food, transport, phone, utilities |

| Wants | 30% | Eating out, entertainment, clothes, apps |

| Savings / Debt Repayment | 20% | Emergency fund, loan payments, savings |

Example with ₹10,000/month:

- ₹5,000 → Needs

- ₹3,000 → Wants

- ₹2,000 → Savings

This isn’t a rigid rule. If you’re living in Mumbai or Delhi and rent takes 60% of your income, that’s your reality — adjust from there. The point is to have some structure.

Zero-Based Budgeting (For When You Want More Control)

The idea here: every single rupee gets a specific job. Income minus all your assigned amounts = zero. Nothing floats around unaccounted for.

It’s more work than 50/30/20. But it gives you total clarity. No surprises at the end of the month. Apps like YNAB are built around this approach if you want to try it.

My honest suggestion: start with 50/30/20. If you want more precision after a month or two, try zero-based. The worst budget is the one sitting in a tab you never open.

→ Related: Best Free Budgeting Apps for Students in 2026 (coming soon)

Setting Financial Goals That Actually Make Sense

Here’s something nobody tells you: saving without a goal feels pointless. You put money aside, and it just sits there feeling abstract.

Goals fix that. They give the money a purpose.

When I started thinking about what I was saving for, it became much easier to actually do it.

Short-Term Goals (This year or next)

These are things you want or need within the next 12 months:

- Build a small emergency fund (even ₹5,000–10,000)

- Replace a broken laptop

- Pay upcoming exam or course fees

- Build up enough to cover one month of expenses

Medium-Term Goals (1–3 years)

- Save for graduation trip or celebration

- Build up funds to move cities for a job

- Pay off a small debt or credit card balance

- Have 3–6 months of expenses saved

Long-Term Goals (3+ years)

- Start a small SIP investment

- Work toward financial independence — not relying on anyone

- Build enough savings to take a risk (quit a bad job, start something)

You don’t need goals in all three categories right now. Just having one short-term goal makes a real difference. Write it down. Give it a number. Put it somewhere you see regularly.

“Save ₹8,000 for a new laptop by December” is more motivating than “save money.” Specific goals work. Vague ones don’t.

How to Save Money as a Student on a Low Income

“I don’t earn enough to save.”

I’ve said this. Most students have said this. And I’m not going to pretend it’s never true — survival mode is real, and some students are genuinely stretched thin.

But a lot of the time, the real issue isn’t the amount. It’s the absence of a system.

Start Ridiculously Small

Don’t try to save 20% right away. Start with an amount so small it barely registers.

₹200 a week. ₹100. Whatever doesn’t feel like a sacrifice.

Set up an automatic transfer — the moment money comes in, a tiny amount moves to a separate savings account before you can spend it. Out of sight, genuinely out of mind.

The habit matters more than the amount right now. Build the habit first, then increase it later.

Build Your Emergency Fund Before Anything Else

Before investing, before any big financial move — build a small buffer.

Students often start with a small emergency fund equal to one or two months of essential expenses and gradually build toward a larger amount over time. For many students, that starting target might be ₹5,000–15,000 depending on your city and lifestyle.

Why? Because without it, every surprise — broken phone, unexpected medical visit, sudden travel — becomes debt. And debt has a way of growing.

One small emergency fund breaks that cycle completely.

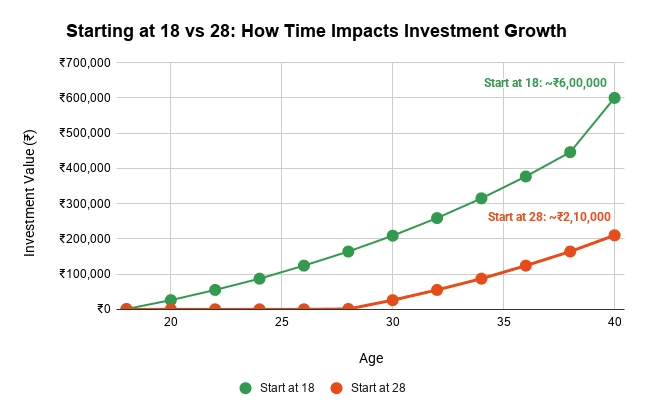

Understand Compound Interest

This is the concept that changed how I think about saving. I’ll keep it short.

When you save money, you earn interest. Next period, you earn interest on the original amount plus the interest from before. That process keeps repeating. Over years, it grows your savings significantly without you doing anything extra.

Here’s a rough example with clear assumptions:

Hypothetical example only — not a guarantee of returns: Monthly investment: ₹1,000 Assumed annual return: 7% Starting at age 18, investing for 22 years (to age 40): Approximate total invested: ₹2,64,000 Approximate value at 40: ~₹6,00,000+

Starting at age 28 instead, for 12 years: Approximate total invested: ₹1,44,000 Approximate value at 40: ~₹2,10,000+

Returns are hypothetical and not guaranteed. Actual results depend on the investment vehicle, market conditions, fees, and timing. Always research before investing.

Disclaimer: Hypothetical example only. Returns are not guaranteed. Actual results depend on the investment vehicle, market conditions, and fees. Always research before investing.

The gap isn’t because the second person is worse with money. It’s just time. That’s compound interest doing its thing.

The NEFE’s financial literacy resources go deeper on this if you want to explore further.

Beginner Investing: Just Enough to Understand It

Once you have even a small emergency fund, it’s worth knowing investing exists — even if you’re not ready to start.

SIPs (Systematic Investment Plans) let you invest a fixed amount every month into a mutual fund automatically. You can start with ₹500/month on platforms like Groww or Zerodha Coin. You don’t need to time the market. You just set a monthly amount and let it run.

Index funds are a common beginner choice — they track a broad market index, costs are usually low, and risk is spread across many companies.

But — and this matters — investing carries real risk. You can lose money. Never invest an amount you’d urgently need back. And do your own research before putting any money in. The Securities and Exchange Board of India (SEBI) has a free investor education portal worth checking before you start.

→ Related: Saving vs Investing: Which Should You Do First? (coming soon)

Banking Basics Every Student Should Know

I assumed everyone just… knew how banking worked. Then I realized I had gaps in my own understanding that I’d never admitted to anyone.

So here’s the straightforward version.

Savings Account vs Current Account

A savings account is what most students use. It earns modest interest on your balance (rates vary by bank). Easy to open, easy to use for day-to-day transactions.

A current account is mainly for businesses. It handles higher transaction volumes but typically earns no interest. As a student, you almost certainly want a savings account — not a current account.

Debit Card vs Credit Card

This one trips a lot of people up.

| Feature | Debit Card | Credit Card |

|---|---|---|

| Where the money comes from | Your own bank balance | The bank lends it to you |

| Spend more than you have? | No — you’re limited to your balance | Yes — up to your credit limit |

| Interest charges? | No | Yes, if you don’t pay full balance monthly |

| Builds credit score? | No | Yes, if used responsibly |

| Risk of debt? | Low | High if misused |

| Good for beginners? | Yes | Yes, but only with discipline |

A debit card spends your own money. A credit card borrows the bank’s money — which you must pay back. This distinction matters more than most people realize.

UPI and Online Banking

In India, UPI (Unified Payments Interface) has made digital payments effortless. PhonePe, Google Pay, Paytm — all use UPI. It’s instant, free, and works 24/7.

Most banks now have solid mobile apps. Set yours up if you haven’t. Being able to check your balance, track transactions, and transfer money instantly makes staying on top of finances much easier.

Avoiding Unnecessary Bank Fees

A few things to watch:

- Minimum balance fees — Some accounts charge you if your balance drops below a certain level. Check your account type. Many student or zero-balance accounts don’t have this.

- ATM charges — Most banks allow a fixed number of free ATM withdrawals per month. Exceeding that incurs small fees that add up.

- SMS alert charges — Some banks charge a small fee for transaction alerts. Check whether yours does.

These are small amounts individually. But noticing them is part of paying attention to your money.

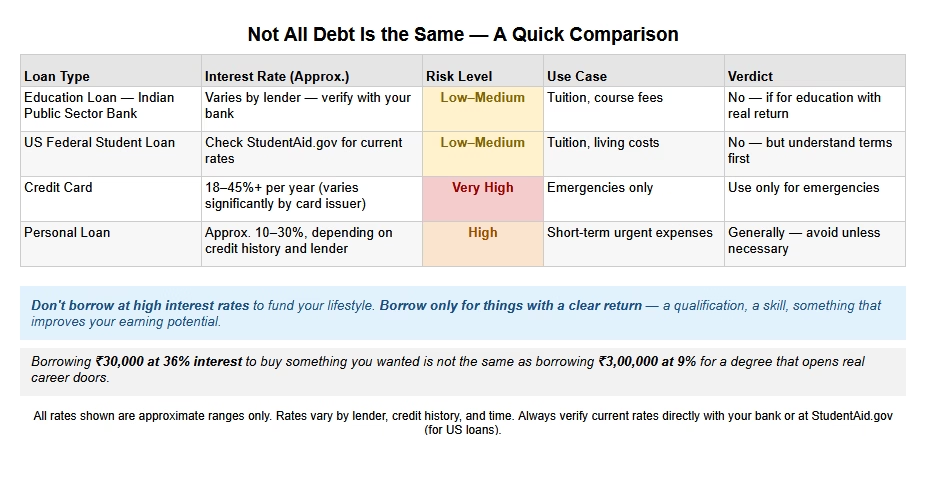

Student Loans: What You Should Know Before You Borrow

Taking a loan for education isn’t automatically a bad decision. For many students, it’s the only realistic path to getting the qualification they want.

But going in without understanding the terms? That’s where things go wrong.

Interest Doesn’t Wait for You to Graduate

Depending on the loan, interest may start building from day one — before you’ve finished studying, before you’ve found a job. By the time your course ends, your balance could be higher than when you started.

Not all loans work this way. Some have a moratorium period — a gap where you don’t have to repay yet. But interest might still be running. Read the terms before signing. All of them.

Not All Debt Is the Same

For US students, StudentAid.gov has clear, up-to-date information on loan types, repayment options, and interest rates directly from the federal government.

For India, the RBI’s Financial Education portal has guidance on banking, savings, and how loan products work.

The Consumer Financial Protection Bureau’s paying-for-college section is also genuinely useful — especially for understanding repayment options after graduation.

The One Rule That Matters Most

Don’t borrow at high interest rates to fund your lifestyle. Borrow for things with a clear return — a qualification, a skill, something that improves your earning potential.

Borrowing ₹30,000 at 36% interest to buy something you wanted is not the same as borrowing ₹3,00,000 at 9% for a degree that opens real career doors.

All rates shown are approximate ranges. Always confirm current rates directly with your lender.

How to Build Credit as a Student Responsibly

Credit felt like an adult concept to me for a long time. Then I realized it starts much earlier than I thought — and that ignoring it early can create headaches later.

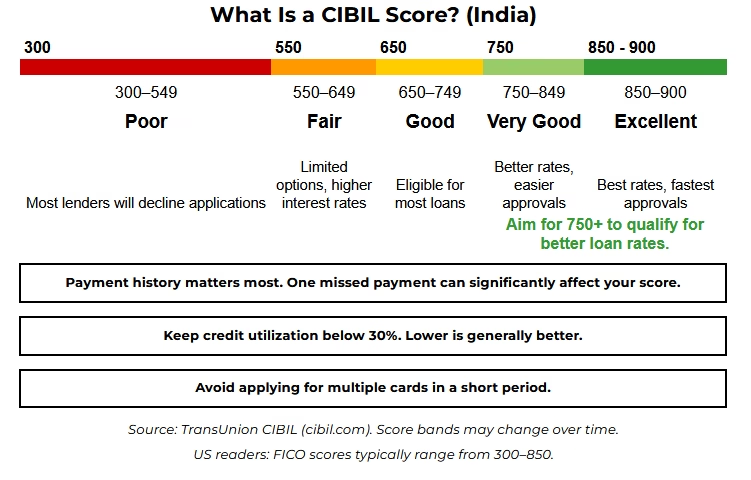

Your credit score is a number that tells banks how reliably you pay back borrowed money.

In India: CIBIL score, range 300–900. In the US: FICO score, range 300–850. Higher = better.

This score affects real things: whether you can rent an apartment, qualify for a loan, or get a better interest rate. It’s built slowly, over time, through consistent behavior.

For more on how the CIBIL score is calculated and what affects it, TransUnion CIBIL’s official site has detailed explanations.

What Goes Into a Credit Score

- Payment history — Do you pay on time? This is the biggest factor.

- Credit utilization — What percentage of your available credit are you using? Many financial educators recommend keeping this below 30%, though lower is generally better.

- Length of credit history — How long have your accounts been open?

- New applications — Have you been applying for credit frequently?

One missed payment can hurt more than months of good behavior helps. Payment history really is that important.

How to Start Building Credit (Without Messing It Up)

1. Get a student or secured credit card. These exist for people with little or no credit history. A secured card is backed by a fixed deposit — the bank’s risk is low, so they’re easier to get.

2. Use it for one small predictable expense. A phone bill. A streaming subscription. Something you’d pay for anyway. Charge it, then pay it immediately.

3. Pay the full balance every single month. Not the minimum — everything. This is non-negotiable. Paying only the minimum triggers interest charges that compound fast. The CFPB has a clear explanation of how credit card interest works if you want to understand the math.

4. Keep utilization low. If your limit is ₹20,000, try to stay below ₹6,000 used at any time.

5. Don’t apply for multiple cards at once. Each application creates a hard inquiry on your record. Multiple hard inquiries in a short window signals financial stress to lenders and can slightly lower your score.

Build it slowly. There’s no shortcut. A clean, consistent track record is the entire goal.

→ Related: What Is a CIBIL Score and How Does It Work? (coming soon)

Common Personal Finance Mistakes Students Should Avoid

These aren’t judgments. They’re just patterns. Almost every student — including me — falls into at least one.

Mistake 1: Treating a Credit Card Like Free Money

It isn’t free. It’s borrowed money with interest attached. If you don’t pay the full balance, that interest compounds fast — often at 18–45% annually, varying by card issuer.

A lot of students build card debt buying things they couldn’t otherwise afford, then spend years slowly paying it off.

Fix: Only spend on a credit card what you already have in your bank account.

Mistake 2: Ignoring Subscriptions

₹149 here. ₹199 there. ₹299 for something you signed up for once and forgot.

Individually harmless. Together, they drain quietly. Six to eight subscriptions can add up to ₹1,200–2,000 a month — money that disappears without you noticing.

Fix: Audit every three months. If you haven’t used something in 30 days, cancel it.

Mistake 3: Having No Emergency Buffer

Something unexpected will happen. Phone screen. Medical visit. Travel emergency. Without a buffer, every surprise becomes debt.

Fix: Build a small emergency fund before anything else. Even ₹3,000–5,000 makes a difference. Students often start small and build it gradually — the goal isn’t perfection, it’s having something.

Mistake 4: Spending to Match Friends

You go places you can’t afford because everyone’s going. You buy things you don’t need because they have them. It’s quiet pressure and it’s real.

Fix: Know your own numbers. Decisions based on your budget, not on how someone else’s life looks on the surface.

Mistake 5: Waiting Until You Earn More

“I’ll start saving when I get a real job.” “I’ll budget once I have a proper income.”

It rarely happens that way. Spending grows with income. The habits you build now follow you forward.

Fix: Start with whatever you have. A small habit built now beats a perfect plan that never starts.

→ Related: Best Side Hustles for Students to Increase Income in 2026 (coming soon)

📋 Disclaimer

Please read this before acting on anything in this article.

This guide is written by a 19-year-old beginner creator for educational and informational purposes only. It is not professional financial, legal, or investment advice.

Interest rates, loan terms, credit rules, and tax laws change regularly and differ by country, bank, and individual situation. All figures and rates mentioned here are approximate and may be outdated by the time you read this.

Always verify current information directly with your bank, a certified financial advisor, or an official government financial resource before making important decisions.

External links are included for reference only. Inclusion of a link does not imply endorsement of the content.

FAQ

What is the best budgeting method for students?

There’s no single best method — it depends on your personality. If you want something simple and flexible, start with the 50/30/20 rule: 50% needs, 30% wants, 20% savings. If you want total control and zero mystery, try zero-based budgeting where every rupee gets assigned a specific purpose. The best method is whichever one you’ll actually stick to.

How much money should students keep in an emergency fund?

Start small. Students often begin with a target equal to one or two months of essential expenses — just enough to handle a broken phone, a medical visit, or a sudden travel need without going into debt. For many students in India, that might be ₹5,000–20,000 depending on their city and lifestyle. Build it gradually. Having something is far better than having nothing.

What’s the difference between a debit card and a credit card?

A debit card spends your own money directly from your bank account. You can only spend what’s there. A credit card borrows money from the bank up to your credit limit — you then have to repay it. If you don’t pay the full balance, interest charges apply, often at high rates. A debit card can’t build your credit score; a credit card can, if used responsibly.

What is the best budgeting method for students with no income?

If you have no income yet, focus on tracking rather than formal budgeting. Note where money comes from and where it goes — even if it’s an allowance from family. Understanding your spending patterns before you earn independently is genuinely useful preparation. Once income starts, even the simplest budget (set aside a fixed percentage first, spend the rest) will put you ahead of most people.

Should students invest before paying off debt?

Generally, no — if the debt carries high interest. Paying off a credit card charging 36% interest gives you a guaranteed 36% return. No investment reliably matches that. The common guidance: clear high-interest debt first, then build an emergency fund, then begin investing. For low-interest debt like an education loan, the calculation is less clear — some people invest and repay simultaneously. But high-interest debt almost always gets paid first.

How much should a student save every month?

There’s no magic number. The common suggestion is 10–20% of income. But if that’s not realistic right now, start with ₹200 or ₹500 — whatever you can move consistently. Consistency matters far more than the amount when you’re building the habit from scratch.

Is it worth getting a credit card as a student in India?

It can be, if you’re disciplined. Student credit cards and secured cards are low-risk ways to begin building a CIBIL score. The one rule that matters: pay the full balance every month, not just the minimum. If you’re not sure you can commit to that, hold off until you are.

Final Thoughts + What To Do This Week

Personal finance for students doesn’t require a finance degree. It doesn’t require a lot of money. It doesn’t require being exceptionally disciplined or organized.

It mostly just requires paying attention.

Knowing where your money goes. Making a rough plan. Saving something, even small. Avoiding high-interest debt. Building credit slowly and cleanly. Setting a goal that makes saving feel like it has a point.

None of that is exciting. None of it goes viral. But it compounds quietly over years — into more options, less financial stress, and more freedom to make choices based on what you actually want rather than what you can currently afford.

Start now. Start small. Stay consistent.

That’s genuinely all there is to it.

✅ What To Do This Week

If you finish reading this and do nothing, you’ll forget most of it by next week. Personal finance for students isn’t about knowing more—it’s about taking small actions consistently. Here are four things you can do in under an hour before the week ends.

- Look at your last 30 days of transactions. Open your bank app right now. Not what you think you spent — what actually happened.

- List every active subscription and its monthly cost. Add them up. You might be surprised.

- Pick one financial goal. Write it down with a number and a date. “Save ₹8,000 by December” beats “save more money.”

- Move a small amount to savings before your next spend. Set up an automatic transfer if possible. Even ₹200 counts.

That’s your starting point. Everything else builds from there.