You know that feeling when you sit down to finally make a budget?

You’ve got your coffee. Your bank statements are open. You’re ready to take control of your money.

Then boom. Confusion hits.

Rent is $1,200 every month. Easy enough. But groceries? Last week you spent $80. The week before, $150. What number do you put in your budget?

And that car insurance bill that shows up twice a year? Where does that go?

Here’s what’s actually happening: You’re trying to budget without understanding the fundamental difference between expenses that stay the same (fixed) and expenses that bounce around (variable). This single gap causes more budget failures than overspending ever will. You can’t control what you can’t categorize.

Most people abandon their budgets within 30 days. Not because they lack discipline. Because they built their budget on a shaky foundation that treats all money the same way.

Understanding fixed vs variable expenses is the secret to building a budget that survives real life. Not a perfect spreadsheet that falls apart after three days. A real system you can actually stick to.

Let’s make this crystal clear before we go deeper.

Fixed Expenses: Costs that stay the same amount every month. They’re predictable and usually locked in by contract, lease, or subscription. You know exactly what you’ll pay before the bill arrives.

Variable Expenses: Costs that change from month to month based on your usage, choices, or circumstances. The amount fluctuates, and you won’t know the final cost until after you’ve spent the money.

Examples: groceries, utilities, gas, dining out, entertainment, clothing, medical expenses

The crucial difference: Fixed expenses represent past commitments you can’t easily change. Variable expenses represent present choices you control daily.

What Fixed Expenses Actually Mean

Think about your rent.

Doesn’t matter if you get a bonus at work or if you’re barely scraping by that month. Your landlord still wants the same amount. That’s a fixed expense.

Fixed expenses stay the same. Month after month. You know exactly what’s coming.

Common fixed expenses include:

Rent or mortgage payments

Car loan payments

Student loan payments

Insurance premiums (health, auto, renters, life)

Phone and internet bills

Subscription services (Netflix, Spotify, gym)

Childcare or tuition

HOA fees

Property taxes

See the pattern? These are commitments you made. Contracts you signed. Services you subscribed to.

Why Fixed Expenses Are Easy (and Hard)

The good news? Fixed expenses are predictable. You can plan around them. You know your car payment is $350, so you make sure $350 is sitting there when the bill comes.

The bad news? They’re sticky. You can’t just cut them in half next month because money’s tight.

Want to lower your rent? You’ve got to move. Want to ditch that car payment? You need to pay off the loan or sell the car.

These changes take time. Sometimes months. Sometimes years.

Quick takeaway: Fixed expenses give you stability but cost you flexibility. They’re the easiest to budget but the hardest to reduce quickly.

What Variable Expenses Really Look Like

Now let’s talk about the expenses that bounce around.

Your electric bill is a perfect example. Run the AC all summer? Maybe you’re paying $150. Nice spring weather where you barely use heating or cooling? Could be $60.

Same bill. Wildly different amounts.

Typical variable expenses:

Groceries

Dining out and takeout

Utilities (electricity, water, gas)

Transportation costs (gas, public transit, ride-shares)

Clothing and personal care

Entertainment

Gifts and celebrations

Home and car repairs

Medical expenses and prescriptions

Pet care

Notice something? These expenses depend on your choices and circumstances.

You control how much you spend on groceries. Whether you meal prep or buy expensive convenience foods. Whether you stick to a list or throw random stuff in your cart.

Why Variable Expenses Get Messy

Here’s the thing. They feel optional even when they’re not.

You have to eat. So groceries aren’t really optional. But spending $200 versus $500? That’s where the choices live.

This flexibility is great. It means you have control. But it also means it’s easy to overspend without noticing.

Most budget disasters happen in the variable expense zone.

Quick takeaway: Variable expenses are where you have the most daily control and the most opportunity to blow your budget. They require active tracking, not just planning.

Key Differences Between Fixed and Variable Expenses

Let’s cut through the textbook stuff and talk about what actually matters.

Characteristic

Fixed Expenses

Variable Expenses

Predictability

You know the exact amount before the bill arrives

You won’t know the final cost until after spending

Flexibility

Difficult to change short-term; requires major decisions

Can adjust immediately with different choices

Budget Method

Assign the exact known amount

Estimate based on past patterns and set a target

Control Level

Low day-to-day control; committed amounts

High day-to-day control; every purchase is a choice

When to Reduce

Requires planning 3-12 months ahead

Can course-correct mid-month

Bottom line: Fixed expenses limit your flexibility. Variable expenses shape your day-to-day spending power.

If you want a deeper understanding of how fixed vs variable expenses work in real life, this helpful budgeting guide explains the differences with simple examples and practical tips you can apply right away. It’s especially useful if you’re trying to figure out where your money actually goes each month and how to gain better control over it.

Real Budgets: How This Plays Out

Let me show you how this works in actual life.

Sarah: Freelance Designer

Her income bounces between $3,000 and $5,000 monthly.

Fixed expenses: $1,850

Rent: $1,200

Car payment: $280

Health insurance: $320

Phone bill: $50

Variable expenses: $1,400 average

Groceries: $300-400

Utilities: $80-120

Gas: $150-200

Dining out: $200-300

Personal care: $100-200

Entertainment: $50-150

Sarah’s strategy: Cover fixed expenses first from every paycheck. Whatever’s left goes to variable categories. In lower-income months, she cuts back on eating out and shopping.

The Martinez Family

Two adults, two kids. Combined income of $7,500 monthly.

Fixed expenses: $4,200

Mortgage: $2,400

Two car payments: $650

Insurance bundle: $420

Internet/streaming: $110

Childcare: $600

Student loan: $320

Variable expenses: $2,400 average

Groceries: $800

Utilities: $250

Gas: $300

Dining out: $250

Kids’ activities: $300

Medical/pharmacy: $200

Home maintenance: $150

Miscellaneous: $150

Remaining: $900

With little breathing room, they’re working on reducing fixed costs by refinancing their mortgage and paying off one car within the year.

Key insight from both examples: Your fixed-to-variable ratio determines your financial flexibility. Higher fixed expenses mean less room to maneuver when income drops or surprise costs hit.

The Grocery Question Everyone Asks

“Are groceries fixed or variable expenses?”

I get this question constantly.

Groceries are variable expenses.

Here’s why people get confused. You have to eat, so groceries feel as essential as rent. Non-negotiable, right?

But unlike rent, the amount changes based on what you buy, where you shop, and whether you waste food.

Some months you stock up on sale items and spend less. Other months you grab expensive pre-made stuff and spend more.

The Smart Approach

Many budgeters treat groceries as semi-fixed. They calculate their three-month average and budget that amount consistently.

This creates predictability while acknowledging the spending might vary by $50 to $100.

Other Confusing Expenses

Utilities? Variable. Usage changes with seasons and habits.

Streaming subscriptions? Fixed. Same price monthly regardless of how much you watch.

Semi-annual car insurance? Still fixed. The amount doesn’t change, just the frequency.

Medical expenses? Variable. You might spend zero one month and $500 the next.

Pet care? Mostly variable (food, vet visits) with some fixed costs (pet insurance).

Reality check: Some expenses live in a gray area. What matters more than the label is how you plan for them in your budget.

How to Build Your Budget Using Both Types

Understanding the difference is great. But how do you actually use this information?

Step 1: Calculate Your Fixed Expense Baseline

Add up everything that stays the same month after month.

This total is your baseline—the absolute minimum you need to function.

Warning sign: If this number exceeds 50% of your take-home pay, you’ve got a problem. You’re locked into commitments that don’t leave enough room for daily living and saving.

Step 2: Analyze Your Variable Spending Patterns

Grab three months of bank statements. Go through them category by category.

Look for:

Your average monthly spending in each category

Patterns (do you always overspend on restaurants?)

Unexpected costs that pop up regularly

Step 3: Set Realistic Variable Targets

Don’t set yourself up to fail. If you’ve spent $400 monthly on groceries for six months straight, don’t budget $200.

Start with your actual averages. Then pick one or two categories where you can reasonably cut back.

Step 4: Build Buffer Money

Life happens. Set aside $200-500 for unexpected variable costs. This isn’t permission to blow your budget. It’s acknowledging reality.

Step 5: Track Weekly, Not Just Monthly

Variable expenses need ongoing attention. Check in every few days.

Spent 80% of your grocery budget by the 15th? Time to get creative with pantry meals for the rest of the month.

Action step: Right now, list every expense you paid last month. Mark each as F (fixed) or V (variable). If you’re not sure, it’s probably variable.

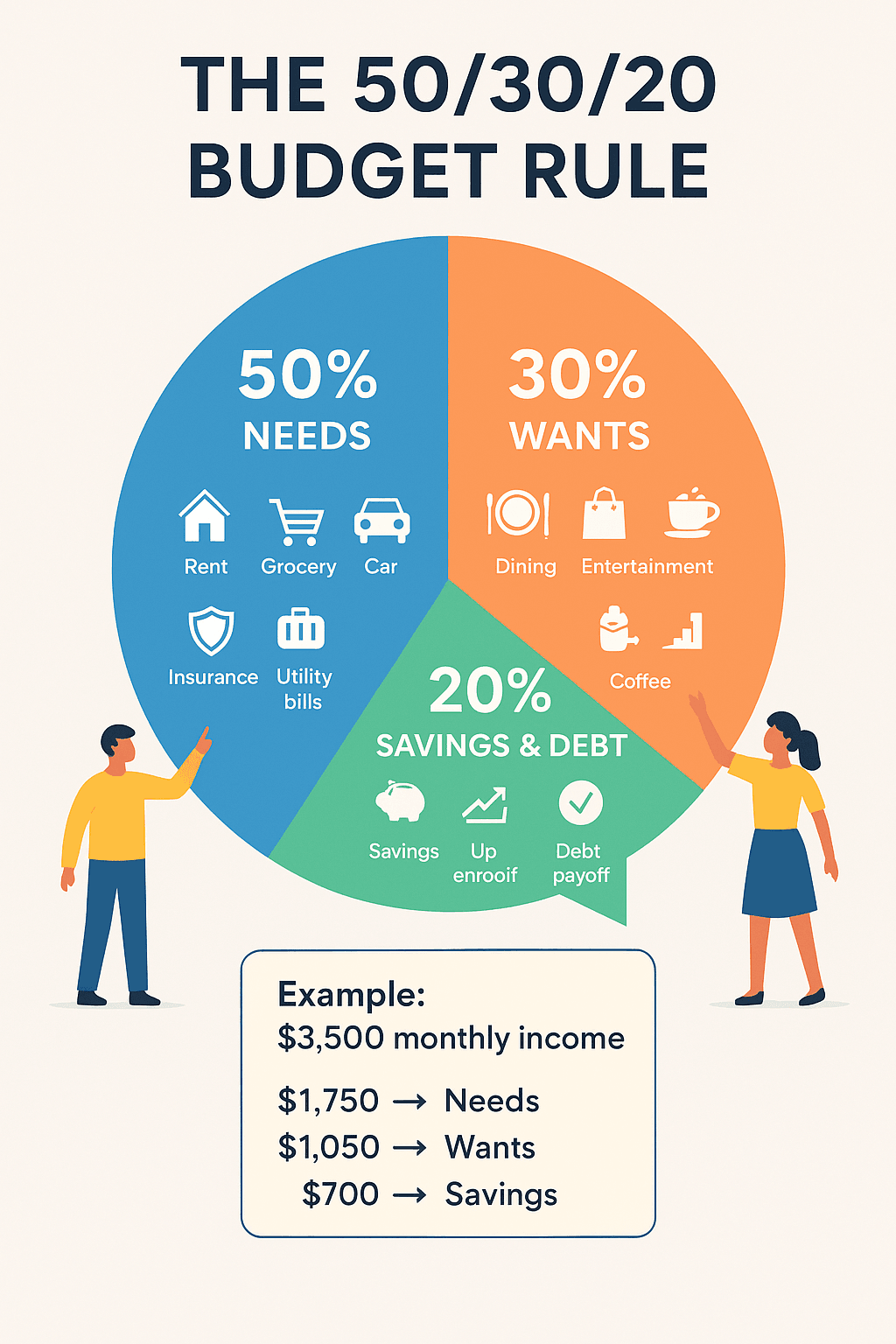

The 50/30/20 Rule (And Why It Sometimes Doesn’t Work)

You’ve probably heard of this budgeting framework:

50% of income → needs

30% → wants

20% → savings and debt

It’s popular because it’s simple. But here’s what most articles don’t tell you.

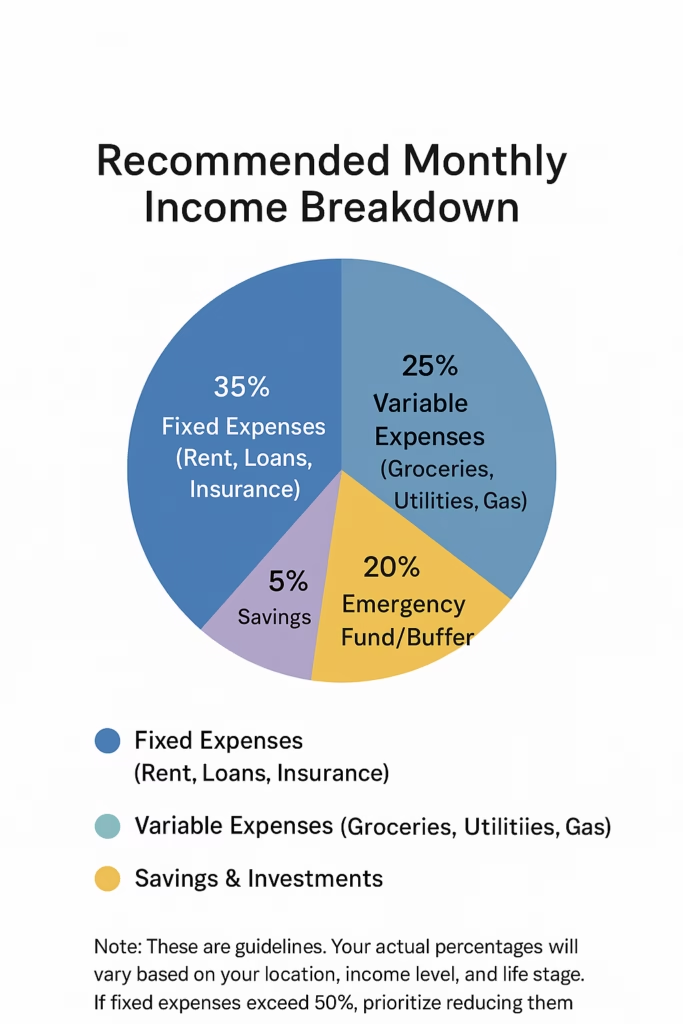

A healthy budget typically allocates 35% to fixed expenses, 25% to variable expenses, 20% to emergency funds, and 20% to savings. If your fixed expenses exceed 50%, prioritize reducing them for better financial flexibility.

Your “savings” (20%) should be treated as fixed: Set up automatic transfers. Treat it like a bill you owe yourself. Don’t wait to see “what’s left” at month’s end.

The Problem

If your fixed expenses alone eat up 70% of your income, this rule won’t work.

You’ll need to tackle those fixed commitments first. Lower the rent by getting a roommate. Pay off a car loan. Cancel subscriptions.

Only then will the 50/30/20 framework become useful.

How to Actually Manage Fixed Expenses

Let’s get tactical.

Audit Your Subscriptions Quarterly

Most people pay for stuff they don’t use. That gym membership you haven’t visited in three months. The streaming service you forgot about.

Go through your bank statements. Cancel anything you’re not actively using.

Even $10 monthly subscriptions add up to $120 yearly.

Negotiate or Shop Around

Fixed expenses feel permanent. But many are negotiable.

Tactics that work:

Call insurance companies and ask for better rates

Check internet and phone plan rates annually

Refinance loans if interest rates dropped

Consider downsizing housing if costs are crushing you

Plan for Irregular Fixed Expenses

Car insurance might hit twice a year. Amazon Prime bills annually. Property taxes come quarterly.

The solution: Take the annual cost, divide by 12, and set aside that amount monthly in a separate savings account.

When the bill comes, you’re ready. No stress.

Limit New Fixed Commitments

Before signing up for any new recurring payment, ask yourself:

Will I use this enough to justify the cost?

Can I commit to this for at least a year?

Every new fixed expense reduces your financial flexibility.

Quick takeaway: Your fixed expenses are yesterday’s decisions affecting today’s flexibility. Review them quarterly and be ruthless about what stays.

How to Actually Manage Variable Expenses

Variable expenses need different tactics.

Use Cash Envelopes (Physical or Digital)

Assign a specific amount to each variable category. When it’s gone, it’s gone.

This creates real constraints. You can’t overspend if the money literally isn’t there.

Don’t want to carry cash? Use a budgeting app that creates virtual envelopes.

Track Spending in Real-Time

Don’t wait until month’s end to check your budget. By then it’s too late.

Check every few days. Quick review. Where do you stand? If you’re running high in one category, pull back immediately.

Identify Your Spending Triggers

Variable expenses often spike because of emotions.

Rough day → ordered takeout

Bored Sunday → browsed online shops

Stressed week → retail therapy

Pay attention to patterns. When do you overspend? Why? Once you understand your triggers, you can interrupt the habit.

Create Simple Spending Rules

Rules reduce decision fatigue:

Only eat out twice a week

Wait 24 hours before buying anything over $50

Meal plan every Sunday to avoid impulse grocery trips

Walk or bike for trips under two miles

No online shopping after 9pm

Use Sinking Funds for Predictable Irregulars

Some variable expenses are unpredictable in timing but totally predictable in happening. Your car will need repairs eventually. Holidays come every year.

Set aside small amounts monthly for these categories. When the expense hits, you’ve got money waiting.

Quick takeaway: Variable expenses are won or lost in the moment. Your system needs to catch overspending before it happens, not after.

Why This Actually Matters

When you don’t separate fixed and variable expenses, you feel powerless. Money just disappears. Bills just happen.

But when you understand the difference, you take back control.

You realize two things:

Fixed expenses are past decisions. Commitments you made months or years ago. You can’t change them today, but you can make a plan to reduce them over time.

Variable expenses are present decisions. Choices you’re making right now. Today. You have power here.

Want to order pizza? That’s a choice. Want to cook the chicken in your fridge instead? Also a choice.

This transforms budgeting from punishment into strategy.

The Financial Freedom Connection

People with financial freedom didn’t all get there by earning six figures.

They managed the relationship between their fixed and variable expenses. They kept fixed expenses low compared to income. This created breathing room. Margin. Space.

That margin becomes savings. That margin becomes the ability to handle emergencies without panic. That margin becomes options.

Options to switch careers. Options to travel. Options to take risks. Options to say no to stuff that doesn’t serve you.

That’s what financial freedom actually is. Not being rich. Having options.

Mistakes People Make (And How to Avoid Them)

Mistake 1: Treating Everything the Same

If you lump all expenses together, you miss the strategic opportunity. You can’t cut your rent this month, but you absolutely can cut restaurant spending.

Fix: Separate your expenses into two columns. Fixed and variable. Right now. You’ll immediately see where your control lives.

Mistake 2: Getting Locked Into Too Many Fixed Expenses

“It’s only $15 a month.” True. But add up ten of those decisions and you’ve committed to $150 monthly that you can’t easily undo.

Fix: Apply the “one-year test.” Before adding any subscription, ask: Will I still want this in 12 months?

Mistake 3: Ignoring Variable Expense Patterns

Just because something varies doesn’t mean you should ignore what you typically spend.

Fix: Calculate three-month averages for each variable category. Use those as your baseline targets.

Mistake 4: Not Planning for Irregular Bills

Annual subscriptions and semi-annual insurance payments blindside people every time.

Fix: List every non-monthly bill you pay. Set up a sinking fund for each one.

Mistake 5: Being Too Rigid With Variable Categories

Life happens. You’ll overspend sometimes. The goal isn’t perfection—it’s awareness and course correction.

Fix: Allow 10% cushion in your variable budget. Use it guilt-free when needed.

Mistake 6: Never Reviewing Fixed Commitments

What made sense two years ago might not make sense now.

Fix: Calendar a quarterly “fixed expense audit.” Review every subscription and recurring bill.

Advanced Moves for When You’ve Got the Basics Down

The 70/20/10 Split for Variable Expenses

Within your variable spending, aim for:

70% on necessities (groceries, utilities, basic transportation)

20% on quality-of-life (reasonable dining out, personal care)

10% on pure fun (entertainment, hobbies)

This prevents you from being either miserable or reckless.

Automate Everything Possible

Set up autopay for fixed expenses. You’ll never miss a due date or pay a late fee.

Set up automatic transfers to savings accounts for irregular fixed expenses.

Automation removes the mental load and the temptation.

Build a One-Month Buffer

Work toward keeping one full month of expenses in your checking account at all times. This means December’s income pays January’s bills.

This buffer eliminates paycheck-to-paycheck stress.

Run Quarterly No-Spend Challenges

Pick one category of variable spending. Do a 30-day challenge. No restaurants. No clothes shopping. No random Amazon purchases.

This resets your baseline, breaks habits, and shows you what you actually need versus what you’ve normalized.

Try Zero-Based Budgeting

Give every dollar a job before the month starts. This works especially well with variable expenses because it forces intentional decisions instead of mindless spending.

How to Cut Costs When You Need To

Sometimes you need to reduce expenses fast. Here’s how.

Cutting Fixed Expenses (Long-Term Strategies)

Housing:

Get a roommate to split costs

Move to a cheaper area or smaller place

Refinance your mortgage if rates dropped

Negotiate rent at lease renewal

Transportation:

Go from two cars to one if possible

Trade in for a cheaper reliable used car

Pay extra toward car loan to eliminate payment faster

Use up pantry and freezer items before buying more

Utilities:

Adjust thermostat a few degrees

Unplug unused devices

Switch to LED bulbs

Take shorter showers

Transportation:

Combine errands into one trip

Carpool when possible

Walk or bike for nearby errands

Maintain your vehicle to prevent expensive repairs

Dining Out:

Set a firm weekly dollar limit

Reserve restaurants for special occasions only

Find free entertainment alternatives

Host potlucks instead of restaurant meetups

Shopping:

Buy only when actually needed, not when bored

Shop secondhand

Learn basic skills (simple alterations, haircuts)

Use products completely before buying new ones

The key: Attack both types simultaneously. Cut variable expenses now for immediate relief. Make a plan to reduce fixed expenses over the next 6-12 months.

Comparison Table: Fixed vs Variable Expenses

Fixed Expenses (Same Every Month)

Variable Expenses (Change Monthly)

🏠 Rent/Mortgage – Same amount locked by lease or loan

🛒 Groceries – Changes based on buying and eating habits

🚗 Car Payment – Fixed installment per loan agreement

🐕 Pet Care & Supplies – Food, vet visits, grooming—varies

Note: Some expenses blur the lines. If you budget the same amount for groceries every month regardless of actual spending, you’re treating it as “semi-fixed” for planning purposes. The key is understanding which expenses you can control immediately (variable) versus those requiring planning to change (fixed).

Quick Answers to Common Questions

What percentage of my income should go to fixed expenses?

Aim for 50% or less of your take-home pay. If you’re over 60%, you’ll struggle to save and handle surprises. The lower your fixed expense percentage, the more flexibility you have.

Can fixed expenses ever change?

Yes, but not easily or often. You can refinance a loan, move to cheaper housing, or cancel subscriptions—but these are deliberate decisions that take effort, not spontaneous adjustments.

How do I budget for unpredictable variable expenses?

Look at your past three months of spending. Calculate your average for each category. Budget slightly higher than that average to give yourself cushion. Track weekly to catch overspending early.

Should I focus on cutting fixed or variable expenses first?

Both matter, different timelines. Cut variable expenses now for immediate results (requires ongoing discipline). Simultaneously, work on a plan to reduce fixed expenses over the next 6-12 months (creates permanent savings).

What if my fixed expenses are way over 50% of my income?

You have three options: increase income, reduce fixed expenses, or both. This might mean taking on extra work, getting a roommate, selling a vehicle, or moving to more affordable housing. Not easy, but necessary for financial stability.

Are credit card payments fixed or variable expenses?

The minimum payment is fixed—you must pay at least that amount monthly. But the total you owe is variable based on your spending. Treat the minimum as fixed in your budget. Put any extra payments in your debt payoff strategy.

How often should I review my budget?

Check variable spending weekly to stay on track. Do a full budget review monthly. Run a deep analysis quarterly to identify patterns, adjust amounts, and look for opportunities to reduce costs.

Is it better to have more fixed or variable expenses?

Neither is inherently better, but lower fixed expenses give you more flexibility. If 70% of your income goes to fixed costs, you’re locked in with little room to adjust. If only 35% is fixed, you have space to save, invest, and handle surprises. Aim for a balance that leaves breathing room.

Take Action: Your Next 24 Hours

Understanding fixed vs variable expenses isn’t about memorizing definitions or perfectly categorizing every transaction.

It’s about building awareness of how your money moves.

Your fixed expenses represent commitments—the life you’ve locked into through leases, loans, and recurring payments. Your variable expenses represent choices—the life you’re creating day by day through small decisions.

Here’s what to do right now:

List your expenses from last month. Every single one.

Mark each as F (fixed) or V (variable).

Add up your fixed expenses and calculate what percentage of your income they consume.

Pick one fixed expense to reduce over the next 90 days (cancel a subscription, shop for better insurance rates, make extra car payments).

Pick one variable category to track closely this week (groceries, dining out, or whatever tends to blow your budget).

That’s it. Five steps. Twenty minutes of work.

This isn’t about building the perfect budget. It’s about taking control through small improvements that compound over time.

Start today.

Go to Next Lesson:

How to Track Your Spending: A Practical Guide That Actually Works

Understanding the difference between fixed and variable expenses is the first step—but knowing where your money actually goes is what turns that knowledge into action. In the next lesson, you’ll learn how to track your spending in a simple, realistic way, so you can spot patterns, control variable expenses, and make better financial decisions without feeling overwhelmed.

For deeper insights into personal finance strategies, certified financial planners and established financial education organizations offer comprehensive budgeting guides and tools. Look for resources that align with your specific financial situation and goals.

I’ll never forget the morning I checked my bank account and saw $47 staring back at me. It was still two weeks until payday. lets talk about this How to Make a Monthly Budget That Actually Works

Here’s the reality: 78% of Americans live paycheck to paycheck, according to recent financial surveys. But here’s what most people don’t realize—you don’t need to earn more money to break this cycle. You just need a system.

Quick Answer: A monthly budget is a simple plan that tracks your income and expenses, helps you prioritize spending, and ensures you’re saving at least 10-20% of your income. Using methods like the 50/30/20 rule or zero-based budgeting, you can take control of your finances in under 30 minutes per week.

This guide is based on 2025 financial best practices from the Consumer Financial Protection Bureau and certified financial planners. Whether you’re trying to build an emergency fund, pay off debt, or simply stop wondering where your money went, this beginner-friendly guide will show you exactly how to create and stick to a budget that works in real life.

Think about it this way: if you were driving cross-country, you’d use GPS, right? You wouldn’t just get in the car and hope you end up in the right place.

Your budget is your financial GPS.

Most people choose monthly budgets because the majority of recurring bills operate on a monthly cycle—rent, utilities, subscriptions, and loan payments all typically come due once per month.

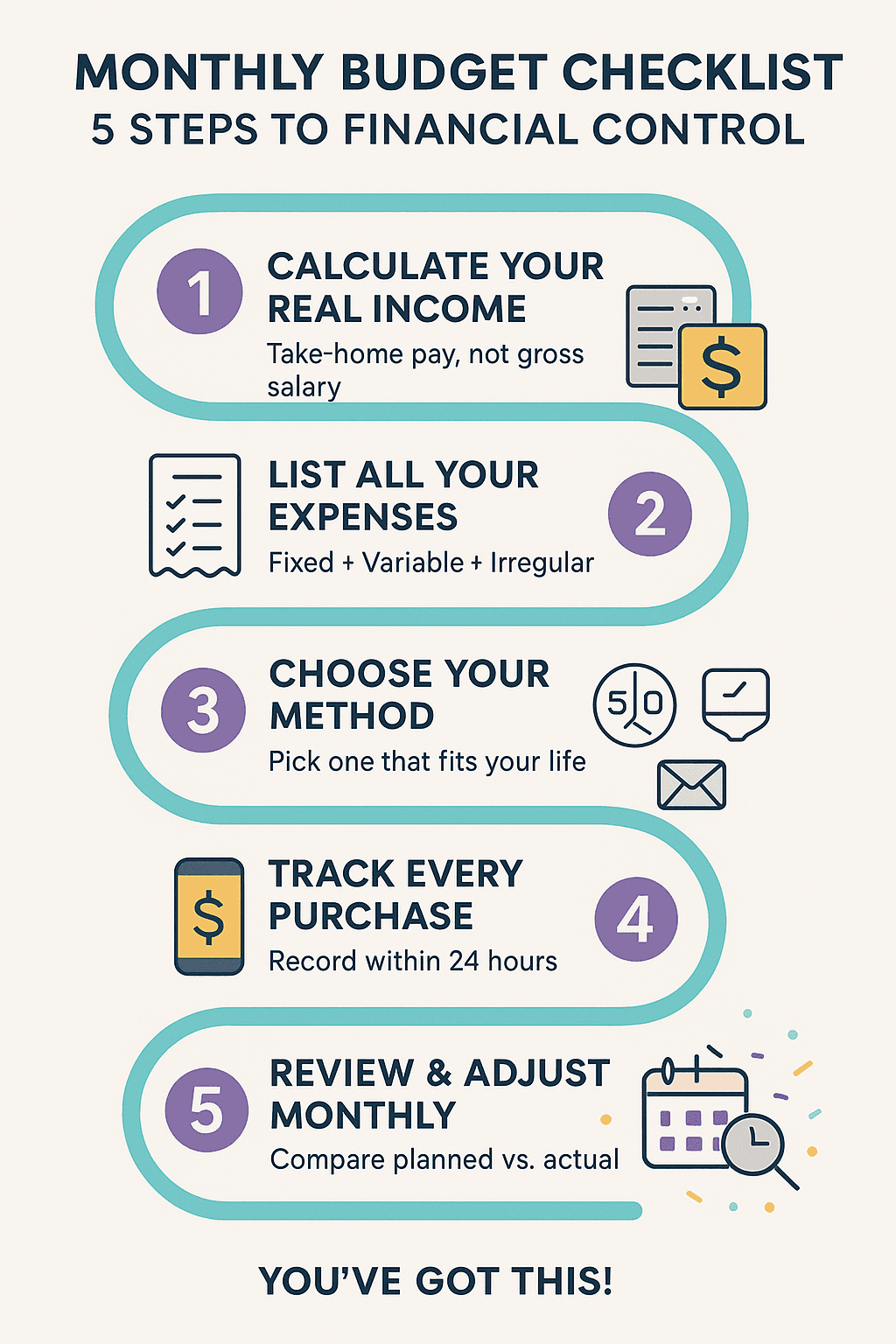

Step 1: Calculate Your Real Take-Home Income (Not Your Salary)

This is where most people mess up right from the start.

They look at their salary and think, “Great, I make $4,000 a month!” But that’s not what hits your bank account.

Find Your Net Income

Net income = Take-home pay after all deductions

Pull up your last few paystubs or check your bank account. Look for the number that actually gets deposited, including deductions for:

Federal and state taxes

Social Security and Medicare

Health insurance premiums

Retirement contributions (401k, IRA)

Other automatic deductions

Example calculation:

Gross monthly salary: $4,500

Taxes and deductions: -$1,100

Net monthly income: $3,400 ← This is your real number

Income Frequency Conversion

Pay Frequency

Calculation Method

Weekly

Multiply by 4.33

Bi-weekly (every 2 weeks)

2 paychecks most months (3 in some months)

Semi-monthly (twice per month)

2 paychecks consistently

Monthly

Use the full amount

Handling Variable or Irregular Income

Freelancer? Server? Commission-based job?

Here’s the safe approach:

Track your income for 3-6 months

Use your lowest-earning month as your baseline budget

During higher-earning months, direct extra income to savings or debt payoff

Create a buffer account to smooth out income variations

Pro tip: Only include side hustle income if it’s reliable and consistent (at least $200+ monthly for 3+ months).

Step 2: Track and Categorize Every Single Expense

This part is eye-opening.

Most of us have no idea how much we actually spend. Time to become a financial detective.

Housing (25-30% maximum): If you’re spending over 35%, consider getting a roommate, downsizing, or increasing income. High housing costs make other financial goals nearly impossible.

Transportation (15-20% maximum): Includes car payments, insurance, gas, maintenance, and public transit. If over 20%, consider refinancing, using public transit more, or downsizing vehicles.

Food:

Single person: $250-400/month for groceries

Family of four: $600-1,000/month

Dining out belongs in discretionary spending, not food budget

Savings (20% minimum): Build emergency fund covering 3-6 months of expenses first, then focus on retirement and long-term goals.

Even with good intentions, these pitfalls sabotage most budgets.

Mistake #1: Using Gross Income Instead of Net

The Problem: Budgeting based on salary before taxes creates a budget with money that doesn’t exist.

Example:

Gross salary: $50,000/year ($4,166/month)

Take-home after taxes: $3,200/month

Gap: $966/month of money that’s not available

Solution: Always budget based on take-home pay (net income).

Mistake #2: Being Unrealistically Restrictive

The Problem: Cutting all enjoyment leads to burnout and spending splurges.

Solution: Include reasonable amounts for entertainment and discretionary spending. It’s better to budget $100 for fun and stick to it than budget $0 and blow $300 in frustration.

Mistake #3: Set It and Forget It

The Problem: Life changes constantly—raises, moves, new babies, paid-off loans. Static budgets become irrelevant.

Solution: Review and adjust quarterly or when significant life changes occur.

Mistake #4: Treating Savings as Optional

The Problem: “I’ll save whatever’s left” means saving nothing.

Solution: Make savings a line item. Automate transfers to savings on payday.

Create dedicated sinking funds for “predictable emergencies”

Add miscellaneous buffer category (5-10% of budget)

Review if “emergencies” could be anticipated (car maintenance, medical)

📋 Compliance & Financial Disclaimer

Important Notice:

The information provided in this article is for educational and informational purposes only and should not be construed as financial advice. Every individual’s financial situation is unique.

Please note:

This content is not a substitute for professional financial planning or advice

Budget recommendations are general guidelines and may not suit your specific circumstances

Tax laws and financial regulations change; consult current IRS guidance for tax-related questions

The author is not a certified financial planner, accountant, or tax professional

Before making significant financial decisions:

Consult with a qualified financial advisor

Review your specific situation with a certified public accountant (CPA)

Consider seeking guidance from a fee-only financial planner

Budget percentages and recommendations are based on widely accepted financial planning principles but may require adjustment for your individual needs, location, and goals.

Accuracy Notice: While every effort has been made to ensure accuracy, financial information and app features may have changed since publication. Verify current details directly with service providers.

Frequently Asked Questions About Monthly Budgeting

How do I make a monthly budget if I’ve never budgeted before?

Start simple: (1) Calculate your take-home income, (2) List all expenses for one month by reviewing bank statements, (3) Use the 50/30/20 rule to allocate 50% to needs, 30% to wants, and 20% to savings. Track spending for the first month without judgment—just observe where money goes. Adjust in month two based on what you learned.

What’s the easiest budgeting method for beginners?

The 50/30/20 rule is the easiest for beginners because it provides clear structure without overwhelming detail. You only need to track three categories instead of dozens. It’s flexible enough to accommodate different lifestyles while ensuring you save at least 20% of income.

How much should I budget for groceries per month?

Grocery budgets vary by location and family size: Single person: $250-400/month, Couple: $400-600/month, Family of four: $600-1,000/month. These are baseline ranges for home cooking. Your actual needs depend on dietary restrictions, local food costs, and eating habits. Track actual spending for 2-3 months to find your realistic number.

Can I create a budget with irregular or variable income?

Yes. Use your lowest-earning month from the past 6 months as your baseline budget. During higher-earning months, direct excess income to savings or debt rather than increasing lifestyle spending. Create a buffer account equal to 1-2 months of expenses to smooth income variations between paychecks.

What budgeting app is best for couples?

Monarch Money is highly rated for couples in 2025 because it offers real-time sync, collaboration features, and the ability for both partners to access and update the budget simultaneously. YNAB and Goodbudget also work well for couples. Choose an app that both partners are willing to use consistently.

How do I stick to a budget when unexpected expenses keep coming up?

Build an emergency fund covering 3-6 months of expenses and create sinking funds for predictable irregular expenses (car maintenance, medical, gifts, annual fees). Add a 5-10% “miscellaneous” buffer category to your monthly budget for truly unexpected costs. Review if your “emergencies” could actually be anticipated and planned for.

Should I pay off debt or save money first?

Build a small emergency fund ($500-1,000) first to avoid going deeper into debt when surprises happen. Then aggressively pay off high-interest debt (credit cards over 15% APR) while maintaining minimum payments on other debts. Once high-interest debt is eliminated, increase emergency fund to 3-6 months of expenses while paying down remaining debt.

Take Control of Your Money Today

Three months from now, you could be looking at your bank account with confidence instead of anxiety.

You could have money saved for the first time in years. You could be making real progress on goals that once felt impossible.

But only if you start.

Here’s your action plan for this week:

Calculate your real take-home income today

Track every expense for 7 days without judgment

Choose one budgeting method to try for 30 days

Set up automatic savings transfer for your next payday

Schedule 15 minutes next Sunday for your first budget review

Remember, your first budget will probably be wrong in several ways. That’s completely normal. Each month teaches you something new about your money habits.

Budgeting isn’t about restriction—it’s about freedom. Freedom to spend confidently on things you value while building the future you want.

Sarah stared at her bank account on her phone, confused. She’d gotten paid just five days ago, and somehow only $47 remained. The bills weren’t even due yet. Where had all her money gone?

If this sounds familiar, you’re not alone. Recent surveys show that nearly half of Americans couldn’t cover their expenses for 90 days. If they lost their income, and one in three has no savings at all. The problem isn’t that people don’t earn enough—it’s that most of us were never taught the fundamental skills of managing money.

Understanding personal finance for beginners doesn’t require a finance degree or complicated spreadsheets. It simply means learning practical strategies to earn, save, spend, and grow your money wisely. Whether you’re 22 or 52, starting your financial education today can transform your entire future.

This comprehensive guide will walk you through everything you need to build a solid financial foundation, avoid costly mistakes, and create the financially secure life you deserve.

Personal finance encompasses every decision you make about money throughout your life. From your first paycheck to your retirement years, how you manage your finances shapes your present circumstances and future possibilities.

Think of personal finance as your financial operating system. Just as your phone needs an operating system to function properly, your life needs a financial system to run smoothly. Without one, you’re essentially winging it—hoping everything works out while leaving yourself vulnerable to unexpected challenges.

The core components of what is personal finance include:

Earning and Income Management: Understanding your take-home pay and maximizing your earning potential through career development and side opportunities.

Spending and Budgeting: Making deliberate choices about where your money goes rather than wondering where it went.

Saving and Emergency Funds: Building a safety net that protects you when life throws curveballs your way.

Debt Management: Understanding the difference between helpful debt and harmful debt, and developing strategies to become debt-free.

Investing and Wealth Building: Growing your money over time through smart investment choices that align with your goals.

Protection and Insurance: Safeguarding your financial future against unexpected events like illness, accidents, or job loss.

Why does mastering these personal finance basics matter so much? Because your relationship with money affects nearly every aspect of your life. Financial stress can damage relationships, harm your health, and prevent you from pursuing your dreams. Conversely, financial confidence opens doors—letting you buy a home, travel, support your family, and retire comfortably.

Research consistently shows that people with basic financial literacy are four times less likely to struggle making ends meet each month. They’re also significantly more prepared for retirement and better equipped to handle economic uncertainty.

The empowering truth is this: personal finance is only about 20% knowledge and 80% behavior. You don’t need to become a financial expert to succeed. You simply need to understand the fundamentals and consistently apply them.

Essential Money Management for Beginners: Building Your Foundation

Money management for beginners starts with understanding where you stand right now. Before you can chart a course to financial success, you need to know your starting point.

Taking Your Financial Snapshot

Begin by gathering all your financial documents: bank statements, credit card bills, loan statements, pay stubs, and any investment accounts. Don’t judge yourself during this process—you’re simply collecting information.

Calculate your total monthly income after taxes. This is your take-home pay, not your gross salary. If you’re paid weekly or biweekly, multiply one paycheck by the number of paychecks you receive annually, then divide by 12 to find your average monthly income.

Next, list all your monthly expenses. Track every single purchase for at least one month—yes, even that $4 coffee. Most people are genuinely surprised when they see their actual spending patterns in black and white. The $10 meal delivery here, the $15 impulse purchase there—these small decisions accumulate into hundreds of dollars monthly.

Categorize your expenses into three groups:

Fixed Expenses: These recurring costs stay relatively consistent—rent or mortgage payments, insurance premiums, car payments, minimum debt payments, and subscriptions.

Variable Necessities: Essential expenses that fluctuate monthly—groceries, utilities, gas, household supplies, and medications.

Discretionary Spending: Non-essential purchases like dining out, entertainment, hobbies, clothing beyond basics, and impulse buys.

This exercise reveals your spending reality, not your perception. You might believe you spend $300 monthly on groceries but discover it’s actually $500 when you include those quick convenience store runs and takeout meals you mentally categorized differently.

Understanding Your Cash Flow

Cash flow simply means the movement of money in and out of your life. Positive cash flow occurs when more money comes in than goes out. Negative cash flow means you’re spending more than you earn—usually through credit cards or loans, which compounds financial problems through interest charges.

Calculate your monthly cash flow with this simple formula:

Monthly Income – Monthly Expenses = Cash Flow

If your result is positive, excellent—you have room to accelerate your financial goals. If it’s zero, you’re living paycheck to paycheck with no buffer for emergencies. If it’s negative, you’re accumulating debt and need immediate action.

Understanding your cash flow isn’t about judgment—it’s about empowerment. You can’t fix problems you don’t know exist, and you can’t celebrate progress without measuring it.

How to Create a Budget That Actually Works

Creating a budget is the single most powerful tool for achieving financial stability and reaching your money goals. Yet the word “budget” makes many people uncomfortable, conjuring images of deprivation and penny-pinching.

Here’s the reality: how to create a budget properly means building a spending plan that reflects your values and priorities while ensuring you cover necessities and build for the future. A good budget shouldn’t feel like a financial straitjacket—it should feel like freedom.

Step-by-Step Budget Creation

Step 1: Calculate Your Monthly Take-Home Income

Start with your actual income—the amount deposited into your account after taxes and deductions. Include all income sources: primary job, side hustles, freelance work, child support, or regular passive income.

For irregular income, review the past three to six months and use the lowest amount as your baseline. This conservative approach prevents overestimating what you’ll earn.

Step 2: List Your Essential Expenses First

Your budget should always prioritize the “Four Walls”—the absolute essentials you need to survive:

Housing (rent/mortgage)

Utilities (electric, water, heat, internet)

Food (groceries, not restaurants)

Transportation (car payment, insurance, gas, or public transit)

Add other non-negotiable expenses: insurance premiums, minimum debt payments, childcare, and medications.

Step 3: Add Your Financial Goals

Before allocating money to discretionary spending, designate funds for:

Treating savings as a bill you must pay ensures it actually happens rather than hoping money remains at month’s end.

Step 4: Allocate Remaining Funds

Now assign the rest to variable expenses and wants:

Groceries and household items

Clothing and personal care

Entertainment and dining out

Hobbies and recreation

Miscellaneous expenses

Be realistic but intentional. If you historically spend $200 monthly on restaurants, don’t budget $50—you’ll fail immediately. Instead, start with $150 and gradually reduce it as you develop new habits.

Step 5: Make Every Dollar Count

Use a zero-based budgeting approach where Income – Expenses = Zero. This doesn’t mean spending everything—it means deliberately assigning every dollar a job. If you have $500 remaining after covering expenses, decide its purpose: $300 to emergency fund, $150 to debt, $50 to fun money.

Choosing Your Budgeting Method

Several effective budgeting frameworks exist. Choose one that matches your personality and lifestyle:

The 50/30/20 Rule: Allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This simple framework works well for beginners who want clear guidelines without excessive tracking.

Zero-Based Budget: Assign every dollar a specific purpose until your income minus expenses equals zero. This method provides maximum control and awareness but requires more detailed tracking.

Envelope System: Withdraw cash for variable spending categories, dividing it into physical or digital envelopes. When an envelope empties, you stop spending in that category. This tangible approach helps visual learners and reformed overspenders.

Pay Yourself First: Automatically transfer savings percentages to separate accounts before spending on anything else. The remainder becomes your spending money without detailed category tracking.

Experiment to find what works. Many people combine approaches—using the 50/30/20 framework with automatic savings transfers and zero-based budgeting for discretionary categories.

Budgeting Method

Best For

How It Works

Pros

Cons

50/30/20 Rule

Beginners who want a simple starting point

50% needs, 30% wants, 20% savings/debt

Easy to follow, flexible

Not ideal for tight incomes

Zero-Based Budgeting

People who want full control

Every rupee/dollar is assigned a job

Maximizes awareness & control

Takes more time to maintain

Envelope System (Digital or Cash)

Overspenders, emotional spenders

Money is divided into categories with limits

Great for controlling impulse spending

Harder to follow digitally

Pay-Yourself-First Method

Anyone trying to build savings fast

Savings are automated before expenses

Builds wealth quickly

Requires discipline to adjust spending

Making Your Budget Stick

Creating a budget takes an hour. Living with one requires consistent effort. These strategies help:

Review weekly: Spend 15 minutes every Sunday reviewing your spending against your budget. Adjust as needed before small problems become big ones.

Use technology: Budgeting apps like EveryDollar, YNAB (You Need a Budget), or Mint automate tracking by connecting to your accounts and categorizing transactions.

Build in flexibility: Life happens. Include a “miscellaneous” category for unexpected small expenses so you’re not constantly revising your entire budget.

Involve your household: If you share finances with a partner, budget together. Shared ownership prevents resentment and ensures both people work toward common goals.

Celebrate milestones: When you successfully stick to your budget for three months or hit a savings target, acknowledge the achievement. Financial discipline deserves recognition.

Remember, your first budget will be imperfect. That’s expected. Each month teaches you more about your actual spending patterns and helps you refine the plan. Progress, not perfection, is the goal.

Financial Planning for Beginners: Setting Goals That Matter

Random acts of saving rarely lead anywhere meaningful. Financial planning for beginners means defining what you actually want money to help you achieve, then creating a roadmap to get there.

Why Financial Goals Matter

Without clear objectives, your budget becomes arbitrary numbers on a spreadsheet rather than a purposeful plan. Goals transform saving from deprivation into intention—you’re not giving up today’s pleasure for nothing; you’re exchanging it for tomorrow’s greater satisfaction.

Research in behavioral psychology shows that people with specific, written financial goals are significantly more likely to achieve them than those with vague aspirations to “save more” or “get out of debt someday.”

Creating SMART Financial Goals

Effective goals follow the SMART framework:

Specific: “Save money” is vague. “Build a $1,000 starter emergency fund” is specific.

Measurable: Quantify your goal so you can track progress. “Save $200 monthly” beats “save when I can.”

Achievable: Stretch yourself, but remain realistic. Saving $2,000 monthly on a $3,000 income isn’t achievable—it’s fantasy.

Relevant: Your goals should align with your values and life circumstances. Don’t pursue someone else’s definition of financial success.

Time-Bound: Set deadlines. “Build emergency fund by December 31” creates urgency that “someday” lacks.

Categorizing Your Goals by Timeline

Financial goals typically fall into three timeframes:

Prioritize ruthlessly. You can’t pursue fifteen goals simultaneously—you’ll spread resources too thin and accomplish nothing. Focus on 2-3 goals at a time, accomplishing them sequentially.

The Priority Order That Works

While everyone’s situation differs, this sequence typically makes sense:

Contribute to retirement accounts (especially if employer matches)

Pay off moderate-interest debt (car loans, student loans)

Save for other goals (house, education, vacations)

Pay off low-interest debt (mortgage) and build wealth

This progression balances security, debt freedom, and long-term growth. Each completed goal creates momentum and frees up money for the next one.

Visualizing and Tracking Progress

Make your goals tangible:

Create a visual tracker—a thermometer chart, progress bar, or jar you fill

Calculate exactly what’s needed: “I need to save $167 monthly for 6 months to reach my $1,000 emergency fund goal”

Celebrate milestones along the way, not just final achievement

Share your goals with an accountability partner

When you connect emotionally with your goals—seeing the beach house you’re saving for or imagining the freedom of being debt-free—you’ll find the discipline to make daily decisions that align with your long-term vision.

How to Build an Emergency Fund for Beginners

Picture this: Your car breaks down on Monday. The repair costs $800. Do you pay with cash, or does this unexpected expense spiral into credit card debt?

This scenario illustrates why building an emergency fund is the cornerstone of financial security. An emergency fund is simply money set aside specifically for unexpected expenses or income loss—your financial safety net.

Why Emergency Funds Are Non-Negotiable

Life’s curveballs are inevitable, not hypothetical. Medical emergencies, job loss, home repairs, car breakdowns—these aren’t questions of if but when. Without savings, each crisis forces you into debt, setting back your financial progress and creating stress.

Research shows that people with emergency savings report significantly lower financial stress and better overall wellbeing. Even having just $2,000 saved can be as powerful for your peace of mind as having $1 million in assets—because it’s immediately accessible when you need it.

How Much Should You Save?

Emergency fund targets depend on your life stage and debt situation:

If you have consumer debt (credit cards, personal loans, anything except your mortgage), start here. This small cushion prevents new debt while you attack existing balances.

One thousand dollars won’t cover every emergency, but it handles most common surprises: a broken appliance, minor car repair, or small medical bill. It’s achievable quickly and provides immediate breathing room.

Once you’re debt-free, build comprehensive protection. Calculate your true monthly living expenses—not your income, but what you actually need to survive: housing, utilities, food, transportation, insurance, and minimum debt payments.

Multiply this by 3-6 months based on:

Lean toward 3 months if: You have stable employment, dual income household, strong job market in your field, no dependents

Lean toward 6+ months if: Self-employed, single income household, unstable industry, several dependents, health concerns, supporting aging parents

For example, if your essential monthly expenses total $3,000, a three-month fund needs $9,000 while a six-month fund requires $18,000.

Where to Keep Your Emergency Fund

Emergency money needs three characteristics: safety, accessibility, and modest growth.,

High-Yield Savings Accounts: These accounts typically offer 4-5% annual interest—significantly better than traditional savings accounts at 0.01%. Your emergency fund should grow while it waits. Online banks usually offer the highest rates.

Money Market Accounts: Similar to savings accounts but may have slightly higher rates and limited check-writing abilities. Generally safe and liquid.

Avoid These Options:

Checking accounts (too accessible for daily spending temptation)

Investment accounts (market volatility could reduce your fund when you need it most)

CDs (penalties for early withdrawal defeat the purpose)

Under your mattress (no growth, not protected against theft/fire)

Separate your emergency fund from your primary checking account. This psychological distance reduces temptation to dip into it for non-emergencies while keeping it accessible within 1-2 business days.

Building Your Fund Without Overwhelm

The full emergency fund number can feel massive and paralyzing. Break it into achievable milestones:

Start with $500: This micro-goal builds momentum and handles many small emergencies.

Reach $1,000: You’ve now got basic protection and can breathe easier.

Hit $2,000: Research shows this amount dramatically improves financial wellbeing.

Continue to full target: Once you’re debt-free, aggressively fund until you reach your 3-6 month goal.

Treat emergency fund contributions like a bill. Set up automatic transfers every payday—even $25 or $50 weekly adds up. You won’t miss money you never see.

Finding Money to Save

“But I have nothing left to save!” is the most common objection. Try these strategies:

Redirect found money: Tax refunds, work bonuses, gift money, or side hustle income goes directly to emergency savings before you’re tempted to spend it.

The savings challenge: Save $1 the first week, $2 the second, $3 the third, and so on. By week 52, you’ll have saved $1,378 with minimal pain.

Cut one thing: Identify one subscription or regular expense you won’t miss. Cancel it and automatically redirect that amount to savings.

Round-up apps: Some banking apps round purchases to the nearest dollar and save the difference. These micro-savings accumulate surprisingly fast.

Challenge yourself: Try a no-spend month on specific categories—no restaurants, no shopping, no entertainment purchases. Bank every dollar you would have spent.

Remember, building your emergency fund isn’t the finish line—it’s the foundation. Once established, you’ll maintain it while pursuing other financial goals. And if you must use it (that’s what it’s for!), immediately begin replenishing it before resuming other savings objectives.

Understanding and Managing Debt Wisely

Debt isn’t inherently evil, but it requires careful management. Understanding how to navigate debt while working toward debt freedom is crucial for personal finance basics.

Good Debt vs. Bad Debt

Not all debt deserves equal urgency in repayment:

Potentially Good Debt:

Mortgage (building equity in an appreciating asset)

Student loans (investing in increased earning potential)

Small business loans (generating income and building assets)

These typically feature lower interest rates and finance things that potentially increase in value or earning capacity.

Financing rapidly depreciating items (furniture, electronics, vehicles beyond your means)

These feature high interest rates and finance consumption rather than investment.

Debt Repayment Strategies

Two primary methods help eliminate debt systematically:

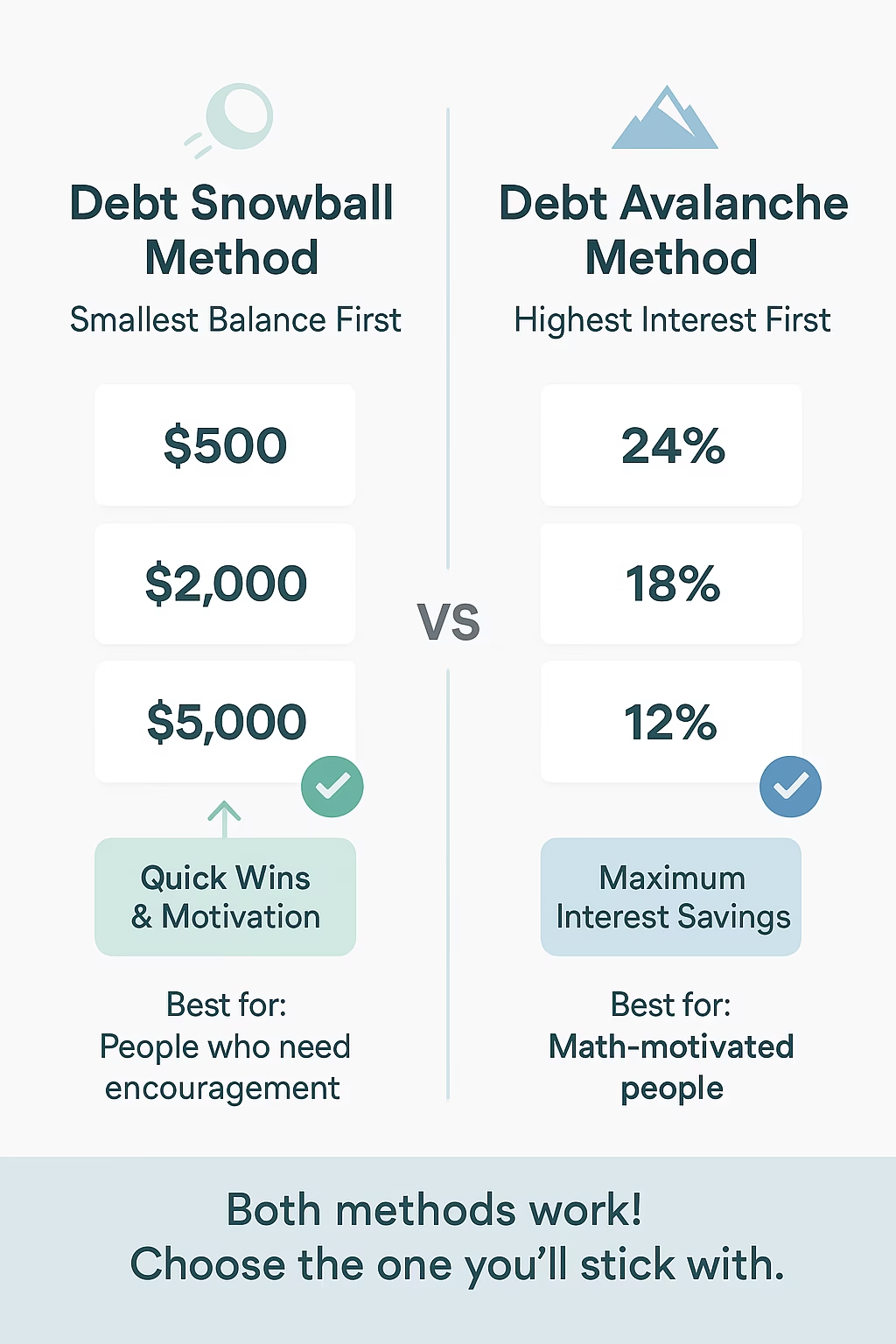

The Debt Snowball: List debts from smallest balance to largest, regardless of interest rate. Pay minimums on everything while attacking the smallest balance with intensity. Once eliminated, roll that payment to the next smallest debt.

This method provides quick psychological wins that build momentum and motivation. Humans respond better to visible progress than mathematical optimization.

The Debt Avalanche: List debts from highest to lowest interest rate. Attack the highest rate first while paying minimums on others.

Mathematically optimal—you’ll pay less interest total and finish faster. However, if you don’t see progress quickly, you might lose motivation before experiencing benefits.

Choose the method matching your personality. Disciplined, patient savers might prefer the avalanche. If you need emotional wins to maintain motivation, use the snowball.

Create free short-term loans when paid in full monthly

Used poorly:

Trap you in high-interest debt cycles

Enable spending beyond your means

Damage credit scores through high utilization or missed payments

Create financial and emotional stress

The golden rule: Only charge what you can pay in full when the statement arrives. If you can’t follow this rule, don’t use credit cards until you develop better spending discipline.

Practical Debt Management Tips

Pay more than minimums: Minimum payments mostly cover interest, barely touching principal. Even an extra $25 monthly significantly accelerates payoff and reduces total interest paid.

Avoid new debt while paying off existing debt: You can’t dig yourself out of a hole while simultaneously digging deeper. Commit to no new debt until current balances are clear.

Negotiate lower rates: Call credit card companies and request lower interest rates, especially if you’ve made consistent on-time payments. Many will agree rather than risk losing you to a balance transfer.

Use windfalls strategically: Tax refunds, bonuses, gifts, or inheritance? Put them toward debt rather than lifestyle inflation.

Track your debt-free date: Calculate exactly when you’ll eliminate debt given your current payment plan. This tangible timeline motivates consistency.

Debt elimination isn’t just mathematical—it’s emotional and psychological. The freedom of owing nothing creates options and reduces stress in ways that compound interest never can.

How to Manage Money Wisely: Daily Habits That Build Wealth

Financial success isn’t about one big decision—it’s about hundreds of small daily choices that compound over time. Learning how to manage money wisely means developing habits that automatically steer you toward financial health.

The 24-Hour Rule

Before any unplanned purchase over $50, wait 24 hours. This cooling-off period reveals whether you truly want something or were experiencing impulse temptation.

Add items to a wish list with the date. Revisit in a week or month. You’ll find many “must-haves” were fleeting desires you’ve completely forgotten about.

Automate Good Behavior

Willpower is finite and unreliable. Automation removes decision fatigue:

Automatic transfers to savings every payday

Automatic retirement contributions

Automatic bill payments (avoiding late fees)

Automatic debt payments above minimums

Set up these systems once, then benefit indefinitely. You’re building wealth without thinking about it.

Practice Conscious Spending

Every purchase is a vote for the life you want. Ask yourself before spending:

Does this align with my values and goals?

Will I care about this in a week? A month? A year?

Is there a less expensive alternative that serves the same purpose?

Am I buying this to solve a real problem or fill an emotional void?

Conscious spending isn’t about deprivation—it’s about intention. Spend lavishly on what you love, cutting mercilessly on what you don’t.

The Weekly Money Date

Schedule 15-30 minutes weekly to review your finances:

Check account balances and recent transactions

Review budget categories and adjust as needed

Update progress toward goals

Address any concerning trends before they become problems

This consistent attention prevents small issues from becoming financial crises and keeps your goals front-of-mind.

Build Financial Margin

Margin is the space between your means and your lifestyle. Living at exactly your income limit leaves no room for life’s variations and opportunities.

Aim to live on 80-90% of your income, saving the rest. This breathing room provides options when unexpected opportunities or challenges arise.

Learn to Say No

Financial health often requires declining requests:

“No, I can’t lend you money”

“No, I can’t go to that expensive restaurant”

“No, I won’t cosign that loan”

“No, I’m not buying rounds tonight”

Your financial wellbeing is more important than temporary social approval. True friends support your goals and respect your boundaries.

Take free online courses about investing, budgeting, or debt management

Follow reputable financial educators on social media

The more you know, the better decisions you’ll make. Financial literacy compounds like interest—early investment pays dividends forever.

Common Personal Finance Mistakes to Avoid

Even well-intentioned people make costly financial errors. Awareness helps you sidestep these common pitfalls.

1. Not Having a Budget

Flying blind financially is the most fundamental mistake. Without tracking income and expenses, you can’t identify problems, make improvements, or measure progress. Even a simple budget beats no budget every time.

2. Living Paycheck to Paycheck by Choice

Some people legitimately struggle with low income, but many live paycheck to paycheck despite earning well. They inflate lifestyle to match income, leaving no margin for emergencies or savings. This lifestyle stress is completely avoidable through conscious spending choices.

3. Ignoring Emergency Funds

Treating emergency funds as optional luxury leaves you vulnerable to spiraling into debt at the first unexpected expense. Without savings, you’re always one crisis away from financial disaster.

4. Paying Only Minimum Payments

Minimum credit card payments primarily cover interest, barely touching principal. You could pay for years while your balance barely drops. Aggressive repayment saves thousands in interest and achieves freedom exponentially faster.

5. Not Understanding Interest

Many people don’t grasp how interest compounds—both for and against them. High-interest debt grows frighteningly fast, while invested money grows surprisingly slow initially. Understanding this math changes behavior dramatically.

6. Co-Signing Loans

When you co-sign, you’re legally responsible for the full debt if the primary borrower defaults. This generous gesture frequently destroys credit scores, depletes savings, and ruins relationships. Support loved ones differently—help them find appropriate loans or improve their credit rather than risking your financial health.

7. Lifestyle Inflation

When income increases, expenses typically rise to match—bigger home, nicer car, expensive hobbies. Instead, banking raises and bonuses accelerates wealth building. Live like you make 10-20% less than actual income.

8. Emotional Spending

Using shopping as therapy, spending when stressed, or making major purchases when emotionally dysregulated leads to regret and debt. Develop non-spending coping mechanisms for emotional needs.

9. Keeping Up with Others

Your neighbor’s new car or friend’s vacation photos shouldn’t dictate your spending. You don’t know their financial situation—they might be drowning in debt behind the Instagram facade. Run your own race based on your values and means.

10. Neglecting Insurance

Skipping health, auto, renters, or life insurance to save money backfires catastrophically when disasters strike. Adequate insurance is protection, not waste. The premiums are minuscule compared to potential uncovered catastrophes.

11. Not Starting Retirement Savings Early

Time is your most powerful wealth-building tool. Starting retirement contributions in your twenties versus your forties can mean hundreds of thousands of dollars difference at retirement due to compound growth. Every year you delay costs you exponentially.

12. Making Investment Decisions Based on Hype

Chasing hot stocks, cryptocurrency trends, or get-rich-quick schemes based on social media buzz rarely ends well. Steady, diversified, long-term investing beats speculation almost always. Boring wins.

Learning from others’ mistakes costs far less than making them yourself. Awareness is half the battle—the other half is choosing differently when temptation strikes.

How to Track Income and Expenses Easily

Tracking spending sounds tedious, but modern tools make it nearly effortless. Without tracking, you’re guessing about your finances rather than knowing.

Manual Tracking Methods

Notebook or Spreadsheet: Old-school but effective. Record every transaction in a simple log. Weekly, categorize expenses and compare to your budget. Requires discipline but provides complete control.

Envelope System: Withdraw monthly cash for variable spending categories. Divide into labeled envelopes—groceries, entertainment, clothing, etc. When an envelope empties, spending in that category stops until next month. Extremely effective for visual learners and those overcoming overspending habits.

Digital Tracking Tools

Budgeting Apps: Applications like Mint, YNAB (You Need A Budget), EveryDollar, and PocketGuard connect to your bank accounts and credit cards, automatically categorizing transactions. You review and approve categorizations rather than manually entering everything.

Bank Tools: Many banks now offer built-in spending categorization and budget tools within their apps. Check if your bank provides these features before downloading separate apps.

Spreadsheet Templates: Google Sheets or Excel templates offer more flexibility than apps while providing calculation automation. Numerous free templates are available online.

Making Tracking Sustainable

Start simple: Track just major categories initially—housing, food, transportation, entertainment. Add detail gradually as the habit solidifies.

Make it routine: Check transactions daily during your morning coffee or evening wind-down. Five minutes daily beats one overwhelming hour weekly.

Use one method consistently: Don’t app-hop constantly. Choose one system and stick with it for at least three months before evaluating effectiveness.

Review patterns monthly: Look for trends. Did restaurant spending increase? Was electricity unusually high? Understanding patterns enables meaningful adjustments.

Don’t judge yourself: Tracking reveals reality, not failure. Use information to improve, not to beat yourself up about past choices.

The goal isn’t perfect tracking—it’s sufficient awareness to make informed financial decisions and catch problems early.

Saving and Investing for Beginners: Building Long-Term Wealth

Saving and investing are different activities serving different purposes. Understanding this distinction is crucial for building comprehensive financial security.

Saving vs. Investing

Saving means setting aside money in safe, liquid accounts for short-term goals and emergencies. Your principal is protected, you can access funds quickly, but growth is modest (currently 4-5% in high-yield savings accounts).

Investing means putting money into assets with growth potential—stocks, bonds, real estate, businesses. Your money can grow substantially over time but involves risk and short-term volatility. Investments are for long-term goals (5+ years away).

The Saving Priority Order

Emergency fund in savings accounts (3-6 months of expenses)

Short-term goal savings (vacation fund, car replacement, home down payment)

High-interest savings accounts for all the above

Beginning Your Investment Journey

Once you have adequate emergency savings and have addressed high-interest debt, investing builds long-term wealth.

Start with Retirement Accounts:

401(k) through Employers: If your company offers 401(k) matching, contribute at least enough to capture the full match—it’s free money. A typical match might be 50% of your contribution up to 6% of salary. Not capturing this match is leaving significant compensation unclaimed.

IRAs (Individual Retirement Accounts): Traditional IRAs provide tax deductions now with taxes paid in retirement. Roth IRAs use after-tax money but grow tax-free forever. For most young people, Roth IRAs offer superior long-term benefits.

Contribution Targets: Aim to invest 10-15% of gross income for retirement. Can’t afford this initially? Start with 3-5% and increase by 1% annually or whenever you get raises.

Investment Basics for Beginners

Diversification is Protection: Don’t put all money in one investment. Spread across different asset types (stocks, bonds) and different companies/sectors. When one investment underperforms, others may compensate.

Index Funds Over Stock Picking: Picking individual stocks is essentially gambling—you’re betting you can predict the future better than millions of other investors. Index funds own tiny pieces of hundreds or thousands of companies, providing instant diversification and matching market returns. Over decades, this approach beats most professional investors.

Time Beats Timing: You cannot reliably predict market highs and lows. Instead of timing the market (impossible), spend time in the market. Long-term, consistent investing beats attempting to perfectly time entry and exit points.

Compound Growth is Magic: Small amounts invested young grow dramatically through decades of compound returns. Invest $200 monthly from age 25-65 at 8% average returns, and you’ll have roughly $700,000. Wait until 35 to start, and you’ll have only about $300,000—half as much despite contributing for 30 years instead of 40.

Starting When You’re Completely New

Robo-Advisors: Platforms like Betterment, Wealthfront, or your bank’s robo-advisor service ask questions about your goals and risk tolerance, then automatically build and manage a diversified portfolio. Perfect for beginners who want professional management without high fees.

Target-Date Funds: These “set it and forget it” funds automatically adjust from aggressive (more stocks) when you’re young to conservative (more bonds) as you approach retirement. Choose the fund closest to your expected retirement year.

Start Small but Start Now: Can’t invest much? Start anyway. Many platforms allow investing with no minimums. Investing $25 monthly teaches valuable lessons while building the habit. Increase contributions as income grows.

Keep Learning: Read beginner investment books, take free online courses, or consult with fee-only financial advisors. Never invest in anything you don’t understand.

The combination of consistent saving for near-term security and strategic investing for long-term growth creates comprehensive financial health. Both deserve attention in your financial plan.

How to Be Financially Responsible in Your 20s (And Beyond)

Your twenties set patterns that echo throughout life. Developing financial responsibility early creates exponential advantages.

Start Retirement Contributions Immediately

“I’m too young to worry about retirement” is perhaps the costliest mistake young adults make. In your twenties, time is your superpower. Money invested at 25 has four decades to compound before retirement—potentially doubling five or six times.

Starting retirement contributions in your twenties versus thirties can create hundreds of thousands of dollars difference despite similar total contributions. This happens because early contributions have so much longer to grow.

Build Credit Thoughtfully

Your credit score affects apartment rentals, car insurance rates, job opportunities, and loan terms for decades. Build it intelligently:

Get a starter credit card and pay the full balance monthly

Keep credit utilization under 30% of limits

Pay all bills on time—set up automatic payments

Check your credit report annually for errors

Don’t close old credit cards (length of history matters)

Live Below Your Means

The gap between what you earn and what you spend determines financial success more than income alone. Someone earning $50,000 who spends $40,000 has more financial power than someone earning $100,000 who spends $105,000.

Resist lifestyle inflation. When you get raises or promotions, bank the increase rather than immediately upgrading your apartment, car, or wardrobe. Living like you make 80% of your actual income creates margin for savings, investing, and handling life’s surprises.

Create Multiple Income Streams

Relying on one income source is risky. Explore side hustles aligned with your skills—freelancing, consulting, online businesses, or gig economy work. Additional income accelerates debt payoff and savings while building skills and reducing dependence on a single employer.

Invest in Yourself

Education, skills, health, and relationships are investments that compound forever. Take courses that increase earning potential. Network intentionally. Maintain physical and mental health—medical bills from neglected health devastate finances.

Your human capital—your ability to earn income—is your most valuable asset in your twenties. Nurture it aggressively.

Avoid Major Financial Mistakes

Certain decisions in your twenties create decade-long consequences:

Don’t accumulate consumer debt for lifestyle inflation

Don’t cosign loans for friends or romantic partners

Don’t skip insurance to save money

Don’t withdraw retirement funds early (penalties and lost growth are devastating)

Don’t make financial decisions to impress others

The freedom to make mistakes is greatest in your twenties because you have time to recover—but why waste years recovering from avoidable errors?

Practice Delayed Gratification

Your twenties present constant temptation—friends’ trips, expensive hobbies, lifestyle upgrades. Learning to delay gratification distinguishes those who build wealth from those who perpetually struggle.

You can have almost anything you want—just not everything simultaneously right now. Prioritize ruthlessly, achieve goals sequentially, and discover that delayed pleasures are often sweeter than instant gratification.

Financial responsibility isn’t about sacrifice—it’s about playing the long game while others sprint aimlessly.

Simple Personal Finance Tips That Make a Big Difference

Small changes compound into significant results. These simple personal finance tips require minimal effort but deliver maximum impact:

Automate Everything Possible

Set up automatic transfers to savings, automatic bill payments, automatic retirement contributions, and automatic debt payments above minimums. Automation removes decision fatigue and prevents forgotten payments.

Use Cash for Problem Categories

If certain spending categories consistently exceed budget—restaurants, shopping, entertainment—switch to cash-only. Physical money creates psychological friction that digital payments lack, naturally reducing overspending.

Implement a Spending Freeze

Choose one category monthly where you spend zero: no restaurants, no shopping, no entertainment purchases. Redirect the savings to financial goals while discovering free or low-cost alternatives.

Unsubscribe Relentlessly

Marketing emails trigger spending impulses. Unsubscribe from promotional emails and abandon shopping apps. You can’t buy what you don’t see.

Calculate Purchases in Work Hours

Before buying something, convert the cost to work hours. That $200 jacket represents 10+ hours of work after taxes. Worth it? Sometimes yes, often no. This mental shift reveals whether purchases align with your values.

Master the Grocery Store

Meal planning, shopping with lists, buying generic brands, and cooking at home are among the highest-return habits. Families easily save $300-500 monthly with improved grocery strategies.

Negotiate Everything

Call service providers annually to negotiate lower rates on internet, phone plans, insurance, and subscriptions. Companies often offer discounts to retain customers—you just need to ask.

Use the Library

Books, movies, music, magazines, online courses, audiobooks—libraries offer massive value absolutely free. Entertainment and education without cost.

Practice the One-In-One-Out Rule

When buying something new, remove something similar you already own. This prevents accumulation while maintaining intentional consumption habits.

Create a Found Money Plan

Decide in advance what you’ll do with windfalls before receiving them. Tax refunds, bonuses, gifts, rebates—these go to financial goals rather than lifestyle inflation. Decide the plan once rather than trusting willpower in the moment.

None of these tips alone transforms finances, but implementing five or six simultaneously creates remarkable momentum.

How to Start Budgeting with Low Income

“Budgeting is for people with money to manage. I’m broke!” This misconception prevents the very people who would benefit most from budgeting from using it.

The truth: budgeting matters more when income is limited. Every dollar must work harder, making intentional allocation critical.

Acknowledge the Reality

Low income creates genuine challenges. Budgeting won’t magically create money that doesn’t exist. However, it ensures every available dollar serves your priorities rather than disappearing into forgotten micro-purchases.

Start with the Four Walls

When money is extremely tight, prioritize these four absolute essentials first:

Food (basic groceries, not restaurants)

Shelter (rent/mortgage and utilities)

Transportation (to work)

Essential clothing and medicine

Everything else comes after these are covered. This prioritization ensures survival while you build toward stability.

Find Every Available Dollar

Cut to Essentials: Eliminate every non-essential expense temporarily—subscriptions, entertainment, dining out, convenience purchases. This isn’t forever, but financial emergencies require intense focus.

Increase Income: Even $10 or $20 weekly from recycling, online surveys, neighborhood services (pet-sitting, lawn care), or selling unused items helps. Small amounts matter significantly at low income levels.