The 5 Money Systems That Transformed My Finances (And Can Change Yours Too)

I used to think managing money just meant saving a little here and there, cutting back on takeout, and hoping I could stick to a budget. But somehow, despite my best efforts, I always felt behind.

Every time I managed to save a bit, life would hit me with something—car trouble, medical bills, a surprise wedding invitation across the country. When I tried investing, I’d end up withdrawing the money just to cover basic expenses. It felt like I was constantly hustling to get ahead, but never actually gaining ground.

It wasn’t until I stopped obsessing over numbers—and started focusing on systems—that everything changed.

Why Systems > Willpower

Most of us try to “fix” our finances with short bursts of efforts : a no-spend month, a new budget app, a viral investing hack. But real financial transformation doesn’t come from hacks—it comes from structure. From money systems that run quietly in the background, supporting your goals even when life gets messy.

Today, my money feels steady—even when things around me aren’t. And I owe that to the five systems I’m about to share with you.

These aren’t rigid rules or complicated spreadsheets. They’re simple, values-based systems that helped me go from stressed and reactive to confident and in control.

Let’s dive into the exact money systems that transformed my financial life—and how you can build them into yours.

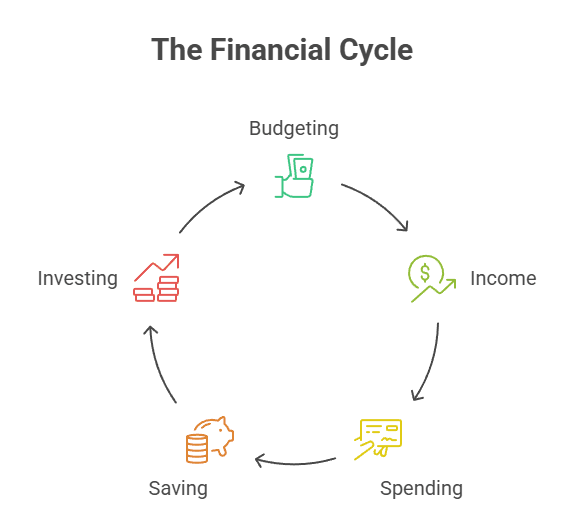

1. The Budgeting System – Clarity Over Control

If you’ve ever tried budgeting and failed, you’re not alone.

I used to see budgeting as punishment—a way to cut joy out of my life and micromanage every penny. It never lasted. What changed everything was switching to a values-based budgeting system.

Instead of tracking every transaction, I focused on the why behind my spending. I asked:

“What do I actually care about?”

“Where do I want my money to go—on purpose?”

That shift created clarity without control. My budget became a reflection of my priorities—not a spreadsheet of shame.

Tools to Try:

- YNAB – Ideal for goal-driven budgeting

- Notion or Google Sheets – Easy to customize around your own categories

- Cash envelope method – If you’re a tactile learner, this keeps spending visible and real

Real-life example: When I labeled my “fun money” category as non-negotiable, I stopped guilt-spending. Ironically, I spent less—because I finally trusted myself.

2. The Income System – Multiple Streams, One Purpose

We’ve all heard the advice: “Earn more!”

Sure. But more income without a system often leads to more chaos.

When I started building multiple income streams—freelance writing, affiliate marketing, and consulting—I quickly realized I needed a way to manage it all. So I built a simple, centralized income system that kept things organized and purposeful.

How I Structured It:

- All income → central business account

- Monthly “owner’s draw” → personal checking

- Automatically route a percentage to taxes, savings, and investments

Pattern break insight:

Imagine your income like a river. It’s not about how wide it is—it’s about where it flows.

More streams mean nothing if they leak out in all directions.

With a system in place, every dollar knows exactly where to go.

3. The Spending System – Conscious, Not Compulsive

Unconscious spending is a silent killer of financial peace. It’s that $7 latte, the “just browsing” online order, the weekend delivery spiral.

To curb this, I implemented a “permission-first” spending system. I automate essentials and financial goals first—so anything left is truly mine to spend guilt-free.

Key Strategies:

- Auto-pay all fixed expenses (rent, insurance, subscriptions)

- Set up automatic savings + investing before money hits checking

- Allocate a fixed “fun money” allowance each month

- Use a 48-hour rule before larger non-essentials

Mindset shift: The goal isn’t to spend less, it’s to spend intentionally. That’s what gives you control and joy.

4. The Saving System – Pay Yourself First (Then Forget It)

Here’s what most people get wrong about saving:

They try to save what’s left after spending.

Spoiler alert: There’s usually nothing left.

That’s why I started paying myself first—automatically. Every time I get paid, a portion goes straight into goal-based savings buckets before I even see it.

How I Do It:

- Auto-transfer to a high-yield savings account

- Create sub-accounts: Emergency Fund, Travel, House Deposit, etc.

- Use apps like Ally, Qapital, or even your bank’s “bucket” system

Visual tip: Label each savings bucket with a goal, not just a dollar amount. “Greece 2025” is way more motivating than “Misc. Savings.”

Even when I couldn’t save much, doing this consistently made me feel empowered—not deprived.

5. The Investing System – Slow, Steady, and Mostly Hands-Off

I used to think investing meant knowing the stock market inside out. I’d stress over headlines, try to time the dips, and constantly second-guess myself.

Now? I invest automatically, monthly, and rarely check the balance.

My System:

- Set up monthly auto-deposit into my brokerage account

- Invest in broad ETFs (like VTI or VXUS)

- Rebalance once a year—maybe

- Let compounding do its thing

Reminder: You don’t need to “beat the market.”

You just need to be in it, consistently.

“Time in the market beats timing the market — every time.” — Warren Buffett

If you’re nervous to start, begin with just $10/month. You’re not trying to get rich quick—you’re building the future in the background.

FAQs

Q: I’m overwhelmed. Where do I start?

Start with one system—budgeting. It’s the foundation. Once you know where your money’s going, it’s easier to optimize the rest.

Q: What if I don’t make a lot of money yet?

These systems scale. Even if you earn ₹15,000/month, you can route 5% to savings or build a basic budget. Consistency > amount.

Q: Is it okay if my system isn’t perfect?

Absolutely. Systems evolve. I tweak mine quarterly. The key is building something that helps you stay intentional.

Final Thoughts: Build the Engine, Not Just the Outcome

The truth is, personal finance doesn’t have to be overwhelming, guilt-ridden, or restrictive.

It can be empowering, aligned, and low-maintenance—if you build the right systems.

Whether you’re freelancing, side hustling, or just trying to make ends meet, these 5 money systems can give you the structure and stability to stop surviving—and start building wealth on your terms.

Ready to stop hustling and start flowing?

Your Turn

Which money system do you already have—or want to build next?

Drop a comment or share this post with a friend who needs a financial refresh.