I still remember sitting in my car outside the grocery store, staring at my bank app in disbelief.

Where did it all go?

I’d gotten paid two weeks earlier, and somehow I was down to $83 in my checking account. Rent was paid, sure. Bills were covered. But everything else? It had just… disappeared.

That’s when I realized I had no idea how to track my spending. Not really. I knew the big stuff—rent, utilities, car payment. But the rest was a complete mystery. Twenty dollars here, forty there, endless small purchases that added up to a massive black hole in my finances.

Learning how to track your spending properly changed everything for me. Not with complicated spreadsheets or guilt-inducing budgets. Just simple, practical tracking that fit into my actual life.

If your money disappears and you don’t know where it goes, this guide will show you exactly what to do—even if you’ve tried tracking before and given up.

That moment when you realize your money is disappearing and you don’t know where it’s going.

Let’s start with the basics.

Tracking your spending means recording every purchase you make and organizing it into categories so you can see patterns, identify waste, and make intentional decisions about where your money goes.

It’s not budgeting. Budgeting is deciding where money should go before you spend it. Tracking is seeing where it actually went after you spent it.

Think of it like this: budgeting is your plan, tracking is your reality check.

Most people skip tracking and jump straight to budgeting. Then they wonder why their budget never works. You can’t build a realistic budget without knowing your actual spending patterns first. If you’re ready to create a budget after tracking, the Consumer Financial Protection Bureau offers a free budget worksheet to get started.

Tracking gives you that foundation. It’s the financial equivalent of turning on the lights in a dark room.

Why Most People Fail at Expense Tracking

Before we get into solutions, let’s talk about why tracking feels so hard.

The biggest reason? Nobody ever taught us how to do it in a way that actually fits into real life.

School didn’t cover it. Personal finance advice assumes you have unlimited time and motivation. Banking apps show transactions, sure, but they don’t help you understand patterns or make better choices.

So most people either:

Try to track perfectly, get overwhelmed, and quit

Use a system that’s too complicated to maintain

Feel too guilty about their spending to look at it

Assume they’re just “bad with money” instead of recognizing they lack visibility

None of these are character flaws. They’re just predictable outcomes when you don’t have a realistic tracking system.

Here’s what actually happens when you don’t track spending:

Small purchases become invisible. That $6 coffee doesn’t register as “spending money.” Neither does the $12 lunch, the $8 snack, or the $15 impulse buy. But together? That’s over $40 in one day that your brain doesn’t count.

Subscriptions multiply silently. You sign up for a free trial, forget to cancel, and suddenly you’re paying $15/month for something you used once. Multiply that by five or six subscriptions and you’re bleeding $75-100 every month.

You can’t tell the difference between a bad week and a bad habit. Did you overspend this week because it was unusual, or because you always overspend? Without tracking, you can’t know.

The result? Constant low-level anxiety about money, even when you’re earning decent income.

How to Track Your Spending for Beginners: Start Simple

Alright, let’s get practical.

The best way to track expenses is whatever method you’ll actually use consistently. The fanciest system in the world is worthless if you abandon it after five days.

Here’s how to start without overwhelming yourself.

Do a Seven-Day Spending Observation

Before you set up any formal system, just observe.

For one week, write down every single thing you spend money on. Everything. Coffee, parking, groceries, bills, that app you downloaded, the tip you left—all of it.

Don’t judge yourself. Don’t try to change anything. Don’t organize it yet. Just collect raw data.

Use whatever’s easiest:

Notes app on your phone

A small notebook in your pocket

Voice memos to yourself

Receipts in an envelope

The tool doesn’t matter at this stage. What matters is capturing every purchase.

This observation week will probably shock you. Most people underestimate their spending by 30-50%. Seeing the actual numbers is eye-opening.

When I did this, I discovered I was spending $180 per month on delivery apps. I would’ve guessed maybe $60. The difference between perception and reality was massive.

Create Five Basic Categories

After your observation week, organize everything into simple categories.

Don’t create 30 categories. Don’t split “groceries” from “food” from “dining out” from “coffee.” That’s how you burn out.

Transportation (gas, public transit, rideshares, parking, car payment)

Daily life (clothing, personal care, phone, internet, household items)

Everything else (entertainment, hobbies, random purchases)

That’s it. Five categories. Simple enough that you’ll actually use them.

You can split categories later if needed. But start simple. Complexity kills habits.

Pick Your Tracking Method

Now choose how you’ll track going forward.

The notebook method: Carry a small notebook. Write down purchases as they happen. Total everything up weekly.

Best for: People who like writing things down and don’t want to rely on technology.

The phone notes method: Keep a running list in your notes app. Add purchases throughout the day. Review weekly.

Best for: People who always have their phone and prefer typing to writing.

The spreadsheet method: Create a simple spreadsheet with columns for date, category, amount, and notes. Update it daily or weekly.

Best for: People who like structure and don’t mind a few minutes of data entry.

The app method: Use a dedicated expense tracking app. Many categorize purchases automatically.

Best for: People who want automation and pretty graphs.

The bank statement method: Review your bank and credit card statements weekly. Highlight and categorize transactions.

Best for: People who use cards for everything and want the simplest possible approach.

I personally use a hybrid system. Quick notes in my phone throughout the day, then I transfer everything to a Google Sheet once a week during Sunday morning coffee. Takes me about eight minutes.

The key is matching the method to your lifestyle, not forcing yourself to use someone else’s “perfect” system.

How to Track Daily Spending Without It Taking Over Your Life

Consistency beats perfection. Here’s how to make tracking sustainable.

Build a Two-Minute Tracking Habit

Tracking should take less than two minutes per day. If it takes longer, you’ll quit.

The trick is capturing purchases immediately, when they’re fresh in your mind.

Create a trigger: Every time you put your wallet away, log the purchase. Every time you’re waiting for a transaction to process, write it down. Every time you get back to your car after shopping, add it to your list.

Connect tracking to something you already do automatically. That’s called habit stacking, and it works because you’re not trying to remember a completely new behavior.

If you forget during the day, set a phone reminder for 8pm. Spend three minutes reviewing your day and catching anything you missed. Check your bank app if you need to jog your memory.

The goal is 85-90% accuracy, not 100%. If you track most purchases, you’ll still see clear patterns. Don’t let perfectionism kill the habit.

Do a Weekly Money Review

This is where tracking becomes powerful.

Every week, sit down for 15 minutes and look at what you spent. Add up each category. Look for patterns.

I do mine every Sunday morning with coffee. It’s become a ritual I actually look forward to, weird as that sounds.

Questions to ask during your review:

What surprises me about this week’s spending?

Where did I spend more than expected?

Were there purchases I regret?

What brought real value to my life?

What could I change next week?

Write down observations. They’re more valuable than the numbers themselves.

This weekly review transforms raw data into understanding. Without it, you’re just collecting numbers that don’t mean anything.

Forgive Missed Days and Keep Going

You will forget to track sometimes. You’ll miss a day, maybe a few days. This is completely normal.

When you realize you missed tracking, just catch up. Don’t spiral into guilt. Don’t start over from scratch. Don’t decide you’ve failed.

Just update what you missed and continue forward.

Most people quit tracking because they miss a few days, feel bad about it, and convince themselves they’re not good at this. That’s nonsense. You just forgot. It happens to everyone. Move on.

Simple Methods to Track Your Spending Throughout the Month

After a few weeks of basic tracking, you’ll start seeing patterns. Now you can refine your approach.

Identify Your Top Three Spending Categories

Look at your data. Which three categories consistently get the most money?

For most people, it’s housing, food, and transportation. But your reality might be different. Maybe it’s food, shopping, and entertainment. Maybe it’s childcare, food, and debt payments.

Whatever your top three are, those deserve the most attention. Small improvements in big categories create bigger results than obsessing over tiny expenses.

When I analyzed my spending, my top three were rent (fixed, couldn’t change), food (way higher than necessary), and random shopping (stuff I didn’t need). Knowing this helped me focus my efforts where they’d actually matter.

Track Variable Expenses More Closely

Some expenses are fixed—rent, insurance, loan payments. They’re the same every month, so you don’t need to track them obsessively. Just verify they happened.

Variable expenses are different every time—groceries, gas, entertainment, shopping. These are where money disappears.

Focus your active tracking energy on variable expenses. That’s where you have control and where patterns emerge.

For fixed expenses, I just have a standing list that I check off monthly. For variable expenses, I track every transaction.

Notice When You Overspend (And Why)

After a month of tracking, patterns become visible.

Maybe you overspend every Friday because you’re exhausted from the work week. Maybe the first week after payday feels like a free-for-all. Maybe you shop when stressed or bored.

These patterns are gold. Once you see them, you can address the actual need instead of just throwing money at it.

I discovered I ordered delivery every time I had a stressful work day. It wasn’t about hunger—it was about comfort and not wanting to deal with one more thing. Once I saw that pattern, I started keeping easy backup meals for those days. My delivery spending dropped by 60%.

Pay attention to emotional triggers, time-based patterns, and situational spending. That’s where the insights live.

How to Monitor Spending Habits: Understanding Your Patterns

Tracking mechanics are important, but understanding what to do with your data matters more.

Compare This Month to Last Month

After two months of tracking, you can start making comparisons.

Did your food spending go up or down? Did you successfully cut entertainment costs? Did a new expense category appear?

Don’t just compare total spending. Compare categories. That’s where you’ll spot trends.

Month-over-month comparison shows whether changes you made actually worked. It also catches gradual increases that would otherwise be invisible.

I noticed my grocery bill had crept up by $40 over three months. Individually, the increases were small. Together, they were significant. Without tracking, I never would’ve caught it.

Separate Wants from Needs (Honestly)

One of the most valuable things tracking does is force honest conversations about wants versus needs.

We tell ourselves lots of stories. “I need this.” “I have to buy that.” “There’s no other option.”

Tracking reveals the truth. You don’t need delivery three times a week. You don’t need the premium version of every subscription. You don’t need most impulse purchases.

That doesn’t mean you should never buy wants. But call them what they are. “I’m choosing to spend $50 on this because I want it” is very different from “I need to spend $50 on this.”

Honest language creates better decisions.

Track Net Worth Changes Alongside Spending

This is more advanced, but powerful.

Every month, calculate your net worth: everything you own minus everything you owe. Write it down. If you’re unfamiliar with the concept, learn how to calculate your net worth and why it matters.

Then compare it to your spending. Are you spending less than you earn? Is your net worth going up?

If your net worth is flat or declining despite tracking, you need to either earn more or reduce fixed expenses. Tracking alone won’t solve that problem, but it will reveal it clearly.

Common Mistakes in Expense Tracking for Beginners

Let me save you from mistakes I made.

Creating Too Many Categories

I started with 23 categories. Twenty-three.

I had separate categories for coffee at home, coffee out, and coffee while traveling. I split entertainment into streaming, events, and hobbies. I differentiated between different types of shopping.

It was insane. I spent more time deciding where purchases belonged than actually tracking them.

Keep categories broad at first. You can always split them later if a category gets too big. But start simple.

Five to eight categories is plenty for beginners.

Only Tracking Big Purchases

Small purchases add up to big totals.

That $4 coffee seems harmless. But 20 of them per month is $80. The $8 lunch five times a week is $160. The $3 snacks add up.

Track everything, especially at first. Small purchases often reveal the biggest opportunities for improvement.

Once you understand your patterns, you can be more selective. But don’t start there.

Waiting for the Perfect System

There is no perfect tracking system. There’s only the system you’ll actually use.

Stop researching apps. Stop watching videos about the ultimate method. Stop waiting for the perfect spreadsheet template.

Start with anything. Literally anything. A napkin works. A text message to yourself works. A voice memo works.

Start imperfectly now instead of perfectly never.

Judging Yourself Harshly

Tracking reveals spending you regret. That’s the point—seeing it helps you avoid it next time.

But beating yourself up doesn’t help. Shame doesn’t create change. It just makes you want to stop tracking.

Observe your spending neutrally, like a scientist collecting data. The numbers aren’t good or bad. They’re just information.

Separate observation from judgment. See what happened, understand why it happened, decide what to do differently. No guilt required.

Practical Steps to Track Your Spending Starting Today

Enough theory. Here’s exactly what to do right now.

Step 1: Write down everything you’ve spent money on today. Right now. Open your phone’s notes app and list it.

Step 2: Set a daily reminder for 8pm. Label it “Track spending.” When it goes off, spend two minutes logging the day’s purchases.

Step 3: Choose one of the tracking methods I described. Pick the simplest one that feels doable.

Step 4: Put a recurring event in your calendar for Sunday mornings called “Weekly money review.” Block 20 minutes.

Step 5: Commit to tracking for one month. Just one. You can quit after that if you hate it.

That’s it. Five concrete actions. Do them today.

Don’t wait for Monday. Don’t wait until the first of the month. Don’t wait until you feel ready.

Start now with whatever you have available.

Tools and Resources (Use What Works for You)

You don’t need fancy tools to track spending effectively. But if you want them, here are options.

For pen and paper people: Any small notebook works. I like ones that fit in a pocket. Moleskine cahiers are nice but a $1 notebook works just as well.

For spreadsheet people: Google Sheets is free and accessible from anywhere. Excel works too. Keep the template simple—date, category, amount, notes. That’s all you need.

For app people: Mint, YNAB (You Need A Budget), PocketGuard, EveryDollar, Goodbudget. Pick one, try it for a month. If you don’t like it, try another. They all track spending, just with different approaches.

If you’re on Android and want something simple for manual tracking, “Buckwheat” is available on the Google Play Store. It’s straightforward, focuses on manual expense entry without automation, and works well for people who want a no-frills approach to logging purchases.

For automatic people: Most banks now offer built-in spending tracking. It’s not perfect at categorization, but it requires zero effort and gives you a starting point.

I know people who’ve transformed their finances with a $1 notebook. I know people with premium apps who still have no idea where their money goes.

The tool matters less than the consistency.

What to Do With Your Tracking Data

Tracking for its own sake doesn’t help much. You need to use what you learn.

Identify One Change Per Month

Look at your data. Pick the easiest problem to solve. Change that one thing.

Maybe it’s canceling a subscription. Maybe it’s packing lunch twice a week. Maybe it’s finding a cheaper option for something you buy regularly.

One change. That’s it. Let it become normal before adding another change.

This might feel slow, but slow actually works. Trying to overhaul everything at once is how you end up changing nothing.

Question Automatic Spending

Tracking reveals purchases you make on autopilot. The same coffee every morning. The same streaming services you barely watch. The same expensive convenience when a cheaper option exists.

Not all automatic spending is bad. But some of it is just habit, not preference.

Question it. “Do I actually want this, or am I just used to buying it?”

Sometimes the answer is yes, you want it. Great. Keep it. But sometimes you realize you don’t care that much, and that awareness changes behavior naturally.

Build Emergency Awareness

Tracking shows you how much you actually need to cover basics. This information is crucial for emergency planning.

If you know your absolute minimum monthly expenses, you know how much emergency savings you need. You know how tight things would get if income dropped. You know which expenses you could cut in a crisis. Use an emergency fund calculator to determine your target savings amount based on your tracked expenses.

This isn’t fun to think about, but it’s important. Tracking gives you the data to plan realistically.

Frequently Asked Questions

How do you track spending if you use cash?

Track it the same way. Write it down as you spend it, or collect receipts and log them later. Cash is actually easier to track in some ways because it’s more tangible and immediate.

What’s the easiest way to track daily expenses for beginners?

The easiest method is the one you’ll actually use. For most people, that’s either a notes app on their phone or a small notebook they keep with them. Start with whichever feels more natural to you.

Should I track my partner’s spending too?

Only if you share finances and they agree to it. If you have joint accounts or shared expenses, tracking together helps. But respect privacy for separate accounts. You can’t force someone else to track if they don’t want to.

How detailed should expense tracking be?

Detailed enough to understand patterns, but not so detailed that tracking becomes a burden. “Groceries $87” is fine. You don’t need to list every item unless you’re trying to optimize grocery spending specifically.

What if I hate looking at my spending because it makes me feel guilty?

This usually means you’re judging yourself too harshly. Try to observe neutrally. The numbers aren’t good or bad—they’re just information that helps you make better decisions. Separate the observation from self-judgment.

Your Next Step: Start Tracking Your Spending Today

You’ve read this far, which means you’re serious about getting control of your money.

Here’s what to do right now:

Open your phone’s notes app. Create a new note called “Spending Log.” Write down everything you’ve purchased today.

That’s it. That’s your first action.

Tomorrow, add tomorrow’s purchases to the list. The day after, do it again.

Do this for one week. Just seven days of writing down what you spend.

After that week, come back to this guide. Follow the steps for choosing a method, creating categories, and setting up your weekly review.

Learning how to track your spending properly is one of the most valuable financial skills you can develop. It’s not exciting, it’s not sexy, but it works.

And it gets easier with time. The habit builds. The patterns become obvious. The decisions become natural.

A few months from now, you’ll look back and wonder how you ever managed money without tracking it. You’ll see your past self stumbling in the dark and feel grateful you finally turned on the lights.

Now that you’ve learned how to track your spending, the next step is protecting your financial progress with a safety net. This lesson breaks down what an emergency fund really is, why it’s essential, and simple strategies to build one that actually works for you.

Sarah stared at her bank account on her phone, confused. She’d gotten paid just five days ago, and somehow only $47 remained. The bills weren’t even due yet. Where had all her money gone?

If this sounds familiar, you’re not alone. Recent surveys show that nearly half of Americans couldn’t cover their expenses for 90 days. If they lost their income, and one in three has no savings at all. The problem isn’t that people don’t earn enough—it’s that most of us were never taught the fundamental skills of managing money.

Understanding personal finance for beginners doesn’t require a finance degree or complicated spreadsheets. It simply means learning practical strategies to earn, save, spend, and grow your money wisely. Whether you’re 22 or 52, starting your financial education today can transform your entire future.

This comprehensive guide will walk you through everything you need to build a solid financial foundation, avoid costly mistakes, and create the financially secure life you deserve.

Personal finance encompasses every decision you make about money throughout your life. From your first paycheck to your retirement years, how you manage your finances shapes your present circumstances and future possibilities.

Think of personal finance as your financial operating system. Just as your phone needs an operating system to function properly, your life needs a financial system to run smoothly. Without one, you’re essentially winging it—hoping everything works out while leaving yourself vulnerable to unexpected challenges.

The core components of what is personal finance include:

Earning and Income Management: Understanding your take-home pay and maximizing your earning potential through career development and side opportunities.

Spending and Budgeting: Making deliberate choices about where your money goes rather than wondering where it went.

Saving and Emergency Funds: Building a safety net that protects you when life throws curveballs your way.

Debt Management: Understanding the difference between helpful debt and harmful debt, and developing strategies to become debt-free.

Investing and Wealth Building: Growing your money over time through smart investment choices that align with your goals.

Protection and Insurance: Safeguarding your financial future against unexpected events like illness, accidents, or job loss.

Why does mastering these personal finance basics matter so much? Because your relationship with money affects nearly every aspect of your life. Financial stress can damage relationships, harm your health, and prevent you from pursuing your dreams. Conversely, financial confidence opens doors—letting you buy a home, travel, support your family, and retire comfortably.

Research consistently shows that people with basic financial literacy are four times less likely to struggle making ends meet each month. They’re also significantly more prepared for retirement and better equipped to handle economic uncertainty.

The empowering truth is this: personal finance is only about 20% knowledge and 80% behavior. You don’t need to become a financial expert to succeed. You simply need to understand the fundamentals and consistently apply them.

Essential Money Management for Beginners: Building Your Foundation

Money management for beginners starts with understanding where you stand right now. Before you can chart a course to financial success, you need to know your starting point.

Taking Your Financial Snapshot

Begin by gathering all your financial documents: bank statements, credit card bills, loan statements, pay stubs, and any investment accounts. Don’t judge yourself during this process—you’re simply collecting information.

Calculate your total monthly income after taxes. This is your take-home pay, not your gross salary. If you’re paid weekly or biweekly, multiply one paycheck by the number of paychecks you receive annually, then divide by 12 to find your average monthly income.

Next, list all your monthly expenses. Track every single purchase for at least one month—yes, even that $4 coffee. Most people are genuinely surprised when they see their actual spending patterns in black and white. The $10 meal delivery here, the $15 impulse purchase there—these small decisions accumulate into hundreds of dollars monthly.

Categorize your expenses into three groups:

Fixed Expenses: These recurring costs stay relatively consistent—rent or mortgage payments, insurance premiums, car payments, minimum debt payments, and subscriptions.

Variable Necessities: Essential expenses that fluctuate monthly—groceries, utilities, gas, household supplies, and medications.

Discretionary Spending: Non-essential purchases like dining out, entertainment, hobbies, clothing beyond basics, and impulse buys.

This exercise reveals your spending reality, not your perception. You might believe you spend $300 monthly on groceries but discover it’s actually $500 when you include those quick convenience store runs and takeout meals you mentally categorized differently.

Understanding Your Cash Flow

Cash flow simply means the movement of money in and out of your life. Positive cash flow occurs when more money comes in than goes out. Negative cash flow means you’re spending more than you earn—usually through credit cards or loans, which compounds financial problems through interest charges.

Calculate your monthly cash flow with this simple formula:

Monthly Income – Monthly Expenses = Cash Flow

If your result is positive, excellent—you have room to accelerate your financial goals. If it’s zero, you’re living paycheck to paycheck with no buffer for emergencies. If it’s negative, you’re accumulating debt and need immediate action.

Understanding your cash flow isn’t about judgment—it’s about empowerment. You can’t fix problems you don’t know exist, and you can’t celebrate progress without measuring it.

How to Create a Budget That Actually Works

Creating a budget is the single most powerful tool for achieving financial stability and reaching your money goals. Yet the word “budget” makes many people uncomfortable, conjuring images of deprivation and penny-pinching.

Here’s the reality: how to create a budget properly means building a spending plan that reflects your values and priorities while ensuring you cover necessities and build for the future. A good budget shouldn’t feel like a financial straitjacket—it should feel like freedom.

Step-by-Step Budget Creation

Step 1: Calculate Your Monthly Take-Home Income

Start with your actual income—the amount deposited into your account after taxes and deductions. Include all income sources: primary job, side hustles, freelance work, child support, or regular passive income.

For irregular income, review the past three to six months and use the lowest amount as your baseline. This conservative approach prevents overestimating what you’ll earn.

Step 2: List Your Essential Expenses First

Your budget should always prioritize the “Four Walls”—the absolute essentials you need to survive:

Housing (rent/mortgage)

Utilities (electric, water, heat, internet)

Food (groceries, not restaurants)

Transportation (car payment, insurance, gas, or public transit)

Add other non-negotiable expenses: insurance premiums, minimum debt payments, childcare, and medications.

Step 3: Add Your Financial Goals

Before allocating money to discretionary spending, designate funds for:

Treating savings as a bill you must pay ensures it actually happens rather than hoping money remains at month’s end.

Step 4: Allocate Remaining Funds

Now assign the rest to variable expenses and wants:

Groceries and household items

Clothing and personal care

Entertainment and dining out

Hobbies and recreation

Miscellaneous expenses

Be realistic but intentional. If you historically spend $200 monthly on restaurants, don’t budget $50—you’ll fail immediately. Instead, start with $150 and gradually reduce it as you develop new habits.

Step 5: Make Every Dollar Count

Use a zero-based budgeting approach where Income – Expenses = Zero. This doesn’t mean spending everything—it means deliberately assigning every dollar a job. If you have $500 remaining after covering expenses, decide its purpose: $300 to emergency fund, $150 to debt, $50 to fun money.

Choosing Your Budgeting Method

Several effective budgeting frameworks exist. Choose one that matches your personality and lifestyle:

The 50/30/20 Rule: Allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This simple framework works well for beginners who want clear guidelines without excessive tracking.

Zero-Based Budget: Assign every dollar a specific purpose until your income minus expenses equals zero. This method provides maximum control and awareness but requires more detailed tracking.

Envelope System: Withdraw cash for variable spending categories, dividing it into physical or digital envelopes. When an envelope empties, you stop spending in that category. This tangible approach helps visual learners and reformed overspenders.

Pay Yourself First: Automatically transfer savings percentages to separate accounts before spending on anything else. The remainder becomes your spending money without detailed category tracking.

Experiment to find what works. Many people combine approaches—using the 50/30/20 framework with automatic savings transfers and zero-based budgeting for discretionary categories.

Budgeting Method

Best For

How It Works

Pros

Cons

50/30/20 Rule

Beginners who want a simple starting point

50% needs, 30% wants, 20% savings/debt

Easy to follow, flexible

Not ideal for tight incomes

Zero-Based Budgeting

People who want full control

Every rupee/dollar is assigned a job

Maximizes awareness & control

Takes more time to maintain

Envelope System (Digital or Cash)

Overspenders, emotional spenders

Money is divided into categories with limits

Great for controlling impulse spending

Harder to follow digitally

Pay-Yourself-First Method

Anyone trying to build savings fast

Savings are automated before expenses

Builds wealth quickly

Requires discipline to adjust spending

Making Your Budget Stick

Creating a budget takes an hour. Living with one requires consistent effort. These strategies help:

Review weekly: Spend 15 minutes every Sunday reviewing your spending against your budget. Adjust as needed before small problems become big ones.

Use technology: Budgeting apps like EveryDollar, YNAB (You Need a Budget), or Mint automate tracking by connecting to your accounts and categorizing transactions.

Build in flexibility: Life happens. Include a “miscellaneous” category for unexpected small expenses so you’re not constantly revising your entire budget.

Involve your household: If you share finances with a partner, budget together. Shared ownership prevents resentment and ensures both people work toward common goals.

Celebrate milestones: When you successfully stick to your budget for three months or hit a savings target, acknowledge the achievement. Financial discipline deserves recognition.

Remember, your first budget will be imperfect. That’s expected. Each month teaches you more about your actual spending patterns and helps you refine the plan. Progress, not perfection, is the goal.

Financial Planning for Beginners: Setting Goals That Matter

Random acts of saving rarely lead anywhere meaningful. Financial planning for beginners means defining what you actually want money to help you achieve, then creating a roadmap to get there.

Why Financial Goals Matter

Without clear objectives, your budget becomes arbitrary numbers on a spreadsheet rather than a purposeful plan. Goals transform saving from deprivation into intention—you’re not giving up today’s pleasure for nothing; you’re exchanging it for tomorrow’s greater satisfaction.

Research in behavioral psychology shows that people with specific, written financial goals are significantly more likely to achieve them than those with vague aspirations to “save more” or “get out of debt someday.”

Creating SMART Financial Goals

Effective goals follow the SMART framework:

Specific: “Save money” is vague. “Build a $1,000 starter emergency fund” is specific.

Measurable: Quantify your goal so you can track progress. “Save $200 monthly” beats “save when I can.”

Achievable: Stretch yourself, but remain realistic. Saving $2,000 monthly on a $3,000 income isn’t achievable—it’s fantasy.

Relevant: Your goals should align with your values and life circumstances. Don’t pursue someone else’s definition of financial success.

Time-Bound: Set deadlines. “Build emergency fund by December 31” creates urgency that “someday” lacks.

Categorizing Your Goals by Timeline

Financial goals typically fall into three timeframes:

Prioritize ruthlessly. You can’t pursue fifteen goals simultaneously—you’ll spread resources too thin and accomplish nothing. Focus on 2-3 goals at a time, accomplishing them sequentially.

The Priority Order That Works

While everyone’s situation differs, this sequence typically makes sense:

Contribute to retirement accounts (especially if employer matches)

Pay off moderate-interest debt (car loans, student loans)

Save for other goals (house, education, vacations)

Pay off low-interest debt (mortgage) and build wealth

This progression balances security, debt freedom, and long-term growth. Each completed goal creates momentum and frees up money for the next one.

Visualizing and Tracking Progress

Make your goals tangible:

Create a visual tracker—a thermometer chart, progress bar, or jar you fill

Calculate exactly what’s needed: “I need to save $167 monthly for 6 months to reach my $1,000 emergency fund goal”

Celebrate milestones along the way, not just final achievement

Share your goals with an accountability partner

When you connect emotionally with your goals—seeing the beach house you’re saving for or imagining the freedom of being debt-free—you’ll find the discipline to make daily decisions that align with your long-term vision.

How to Build an Emergency Fund for Beginners

Picture this: Your car breaks down on Monday. The repair costs $800. Do you pay with cash, or does this unexpected expense spiral into credit card debt?

This scenario illustrates why building an emergency fund is the cornerstone of financial security. An emergency fund is simply money set aside specifically for unexpected expenses or income loss—your financial safety net.

Why Emergency Funds Are Non-Negotiable

Life’s curveballs are inevitable, not hypothetical. Medical emergencies, job loss, home repairs, car breakdowns—these aren’t questions of if but when. Without savings, each crisis forces you into debt, setting back your financial progress and creating stress.

Research shows that people with emergency savings report significantly lower financial stress and better overall wellbeing. Even having just $2,000 saved can be as powerful for your peace of mind as having $1 million in assets—because it’s immediately accessible when you need it.

How Much Should You Save?

Emergency fund targets depend on your life stage and debt situation:

If you have consumer debt (credit cards, personal loans, anything except your mortgage), start here. This small cushion prevents new debt while you attack existing balances.

One thousand dollars won’t cover every emergency, but it handles most common surprises: a broken appliance, minor car repair, or small medical bill. It’s achievable quickly and provides immediate breathing room.

Once you’re debt-free, build comprehensive protection. Calculate your true monthly living expenses—not your income, but what you actually need to survive: housing, utilities, food, transportation, insurance, and minimum debt payments.

Multiply this by 3-6 months based on:

Lean toward 3 months if: You have stable employment, dual income household, strong job market in your field, no dependents

Lean toward 6+ months if: Self-employed, single income household, unstable industry, several dependents, health concerns, supporting aging parents

For example, if your essential monthly expenses total $3,000, a three-month fund needs $9,000 while a six-month fund requires $18,000.

Where to Keep Your Emergency Fund

Emergency money needs three characteristics: safety, accessibility, and modest growth.,

High-Yield Savings Accounts: These accounts typically offer 4-5% annual interest—significantly better than traditional savings accounts at 0.01%. Your emergency fund should grow while it waits. Online banks usually offer the highest rates.

Money Market Accounts: Similar to savings accounts but may have slightly higher rates and limited check-writing abilities. Generally safe and liquid.

Avoid These Options:

Checking accounts (too accessible for daily spending temptation)

Investment accounts (market volatility could reduce your fund when you need it most)

CDs (penalties for early withdrawal defeat the purpose)

Under your mattress (no growth, not protected against theft/fire)

Separate your emergency fund from your primary checking account. This psychological distance reduces temptation to dip into it for non-emergencies while keeping it accessible within 1-2 business days.

Building Your Fund Without Overwhelm

The full emergency fund number can feel massive and paralyzing. Break it into achievable milestones:

Start with $500: This micro-goal builds momentum and handles many small emergencies.

Reach $1,000: You’ve now got basic protection and can breathe easier.

Hit $2,000: Research shows this amount dramatically improves financial wellbeing.

Continue to full target: Once you’re debt-free, aggressively fund until you reach your 3-6 month goal.

Treat emergency fund contributions like a bill. Set up automatic transfers every payday—even $25 or $50 weekly adds up. You won’t miss money you never see.

Finding Money to Save

“But I have nothing left to save!” is the most common objection. Try these strategies:

Redirect found money: Tax refunds, work bonuses, gift money, or side hustle income goes directly to emergency savings before you’re tempted to spend it.

The savings challenge: Save $1 the first week, $2 the second, $3 the third, and so on. By week 52, you’ll have saved $1,378 with minimal pain.

Cut one thing: Identify one subscription or regular expense you won’t miss. Cancel it and automatically redirect that amount to savings.

Round-up apps: Some banking apps round purchases to the nearest dollar and save the difference. These micro-savings accumulate surprisingly fast.

Challenge yourself: Try a no-spend month on specific categories—no restaurants, no shopping, no entertainment purchases. Bank every dollar you would have spent.

Remember, building your emergency fund isn’t the finish line—it’s the foundation. Once established, you’ll maintain it while pursuing other financial goals. And if you must use it (that’s what it’s for!), immediately begin replenishing it before resuming other savings objectives.

Understanding and Managing Debt Wisely

Debt isn’t inherently evil, but it requires careful management. Understanding how to navigate debt while working toward debt freedom is crucial for personal finance basics.

Good Debt vs. Bad Debt

Not all debt deserves equal urgency in repayment:

Potentially Good Debt:

Mortgage (building equity in an appreciating asset)

Student loans (investing in increased earning potential)

Small business loans (generating income and building assets)

These typically feature lower interest rates and finance things that potentially increase in value or earning capacity.

Financing rapidly depreciating items (furniture, electronics, vehicles beyond your means)

These feature high interest rates and finance consumption rather than investment.

Debt Repayment Strategies

Two primary methods help eliminate debt systematically:

The Debt Snowball: List debts from smallest balance to largest, regardless of interest rate. Pay minimums on everything while attacking the smallest balance with intensity. Once eliminated, roll that payment to the next smallest debt.

This method provides quick psychological wins that build momentum and motivation. Humans respond better to visible progress than mathematical optimization.

The Debt Avalanche: List debts from highest to lowest interest rate. Attack the highest rate first while paying minimums on others.

Mathematically optimal—you’ll pay less interest total and finish faster. However, if you don’t see progress quickly, you might lose motivation before experiencing benefits.

Choose the method matching your personality. Disciplined, patient savers might prefer the avalanche. If you need emotional wins to maintain motivation, use the snowball.

Create free short-term loans when paid in full monthly

Used poorly:

Trap you in high-interest debt cycles

Enable spending beyond your means

Damage credit scores through high utilization or missed payments

Create financial and emotional stress

The golden rule: Only charge what you can pay in full when the statement arrives. If you can’t follow this rule, don’t use credit cards until you develop better spending discipline.

Practical Debt Management Tips

Pay more than minimums: Minimum payments mostly cover interest, barely touching principal. Even an extra $25 monthly significantly accelerates payoff and reduces total interest paid.

Avoid new debt while paying off existing debt: You can’t dig yourself out of a hole while simultaneously digging deeper. Commit to no new debt until current balances are clear.

Negotiate lower rates: Call credit card companies and request lower interest rates, especially if you’ve made consistent on-time payments. Many will agree rather than risk losing you to a balance transfer.

Use windfalls strategically: Tax refunds, bonuses, gifts, or inheritance? Put them toward debt rather than lifestyle inflation.

Track your debt-free date: Calculate exactly when you’ll eliminate debt given your current payment plan. This tangible timeline motivates consistency.

Debt elimination isn’t just mathematical—it’s emotional and psychological. The freedom of owing nothing creates options and reduces stress in ways that compound interest never can.

How to Manage Money Wisely: Daily Habits That Build Wealth

Financial success isn’t about one big decision—it’s about hundreds of small daily choices that compound over time. Learning how to manage money wisely means developing habits that automatically steer you toward financial health.

The 24-Hour Rule

Before any unplanned purchase over $50, wait 24 hours. This cooling-off period reveals whether you truly want something or were experiencing impulse temptation.

Add items to a wish list with the date. Revisit in a week or month. You’ll find many “must-haves” were fleeting desires you’ve completely forgotten about.

Automate Good Behavior

Willpower is finite and unreliable. Automation removes decision fatigue:

Automatic transfers to savings every payday

Automatic retirement contributions

Automatic bill payments (avoiding late fees)

Automatic debt payments above minimums

Set up these systems once, then benefit indefinitely. You’re building wealth without thinking about it.

Practice Conscious Spending

Every purchase is a vote for the life you want. Ask yourself before spending:

Does this align with my values and goals?

Will I care about this in a week? A month? A year?

Is there a less expensive alternative that serves the same purpose?

Am I buying this to solve a real problem or fill an emotional void?

Conscious spending isn’t about deprivation—it’s about intention. Spend lavishly on what you love, cutting mercilessly on what you don’t.

The Weekly Money Date

Schedule 15-30 minutes weekly to review your finances:

Check account balances and recent transactions

Review budget categories and adjust as needed

Update progress toward goals

Address any concerning trends before they become problems

This consistent attention prevents small issues from becoming financial crises and keeps your goals front-of-mind.

Build Financial Margin

Margin is the space between your means and your lifestyle. Living at exactly your income limit leaves no room for life’s variations and opportunities.

Aim to live on 80-90% of your income, saving the rest. This breathing room provides options when unexpected opportunities or challenges arise.

Learn to Say No

Financial health often requires declining requests:

“No, I can’t lend you money”

“No, I can’t go to that expensive restaurant”

“No, I won’t cosign that loan”

“No, I’m not buying rounds tonight”

Your financial wellbeing is more important than temporary social approval. True friends support your goals and respect your boundaries.

Take free online courses about investing, budgeting, or debt management

Follow reputable financial educators on social media

The more you know, the better decisions you’ll make. Financial literacy compounds like interest—early investment pays dividends forever.

Common Personal Finance Mistakes to Avoid

Even well-intentioned people make costly financial errors. Awareness helps you sidestep these common pitfalls.

1. Not Having a Budget

Flying blind financially is the most fundamental mistake. Without tracking income and expenses, you can’t identify problems, make improvements, or measure progress. Even a simple budget beats no budget every time.

2. Living Paycheck to Paycheck by Choice

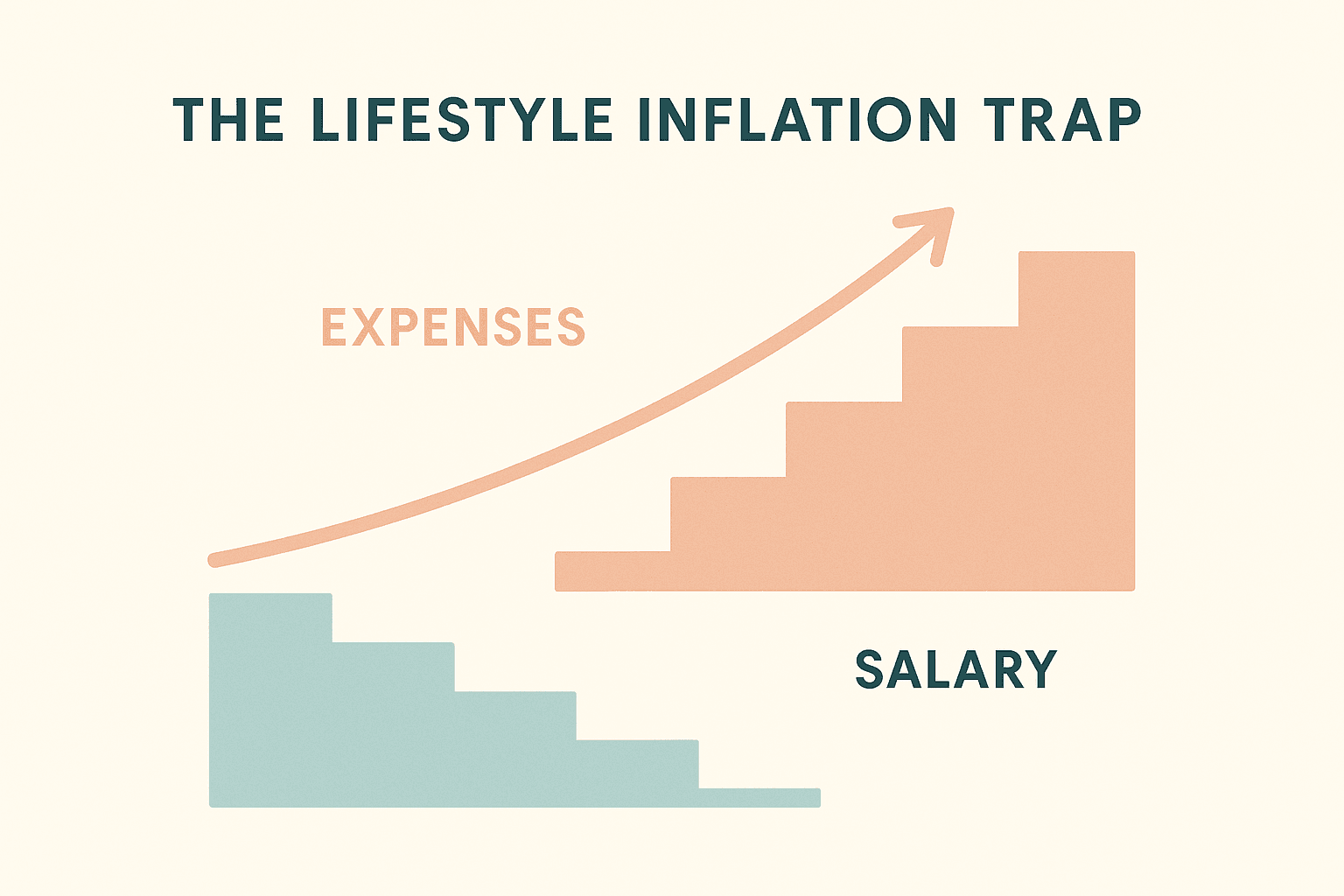

Some people legitimately struggle with low income, but many live paycheck to paycheck despite earning well. They inflate lifestyle to match income, leaving no margin for emergencies or savings. This lifestyle stress is completely avoidable through conscious spending choices.

3. Ignoring Emergency Funds

Treating emergency funds as optional luxury leaves you vulnerable to spiraling into debt at the first unexpected expense. Without savings, you’re always one crisis away from financial disaster.

4. Paying Only Minimum Payments

Minimum credit card payments primarily cover interest, barely touching principal. You could pay for years while your balance barely drops. Aggressive repayment saves thousands in interest and achieves freedom exponentially faster.

5. Not Understanding Interest

Many people don’t grasp how interest compounds—both for and against them. High-interest debt grows frighteningly fast, while invested money grows surprisingly slow initially. Understanding this math changes behavior dramatically.

6. Co-Signing Loans

When you co-sign, you’re legally responsible for the full debt if the primary borrower defaults. This generous gesture frequently destroys credit scores, depletes savings, and ruins relationships. Support loved ones differently—help them find appropriate loans or improve their credit rather than risking your financial health.

7. Lifestyle Inflation

When income increases, expenses typically rise to match—bigger home, nicer car, expensive hobbies. Instead, banking raises and bonuses accelerates wealth building. Live like you make 10-20% less than actual income.

8. Emotional Spending

Using shopping as therapy, spending when stressed, or making major purchases when emotionally dysregulated leads to regret and debt. Develop non-spending coping mechanisms for emotional needs.

9. Keeping Up with Others

Your neighbor’s new car or friend’s vacation photos shouldn’t dictate your spending. You don’t know their financial situation—they might be drowning in debt behind the Instagram facade. Run your own race based on your values and means.

10. Neglecting Insurance

Skipping health, auto, renters, or life insurance to save money backfires catastrophically when disasters strike. Adequate insurance is protection, not waste. The premiums are minuscule compared to potential uncovered catastrophes.

11. Not Starting Retirement Savings Early

Time is your most powerful wealth-building tool. Starting retirement contributions in your twenties versus your forties can mean hundreds of thousands of dollars difference at retirement due to compound growth. Every year you delay costs you exponentially.

12. Making Investment Decisions Based on Hype

Chasing hot stocks, cryptocurrency trends, or get-rich-quick schemes based on social media buzz rarely ends well. Steady, diversified, long-term investing beats speculation almost always. Boring wins.

Learning from others’ mistakes costs far less than making them yourself. Awareness is half the battle—the other half is choosing differently when temptation strikes.

How to Track Income and Expenses Easily

Tracking spending sounds tedious, but modern tools make it nearly effortless. Without tracking, you’re guessing about your finances rather than knowing.

Manual Tracking Methods

Notebook or Spreadsheet: Old-school but effective. Record every transaction in a simple log. Weekly, categorize expenses and compare to your budget. Requires discipline but provides complete control.

Envelope System: Withdraw monthly cash for variable spending categories. Divide into labeled envelopes—groceries, entertainment, clothing, etc. When an envelope empties, spending in that category stops until next month. Extremely effective for visual learners and those overcoming overspending habits.

Digital Tracking Tools

Budgeting Apps: Applications like Mint, YNAB (You Need A Budget), EveryDollar, and PocketGuard connect to your bank accounts and credit cards, automatically categorizing transactions. You review and approve categorizations rather than manually entering everything.

Bank Tools: Many banks now offer built-in spending categorization and budget tools within their apps. Check if your bank provides these features before downloading separate apps.

Spreadsheet Templates: Google Sheets or Excel templates offer more flexibility than apps while providing calculation automation. Numerous free templates are available online.

Making Tracking Sustainable

Start simple: Track just major categories initially—housing, food, transportation, entertainment. Add detail gradually as the habit solidifies.

Make it routine: Check transactions daily during your morning coffee or evening wind-down. Five minutes daily beats one overwhelming hour weekly.

Use one method consistently: Don’t app-hop constantly. Choose one system and stick with it for at least three months before evaluating effectiveness.

Review patterns monthly: Look for trends. Did restaurant spending increase? Was electricity unusually high? Understanding patterns enables meaningful adjustments.

Don’t judge yourself: Tracking reveals reality, not failure. Use information to improve, not to beat yourself up about past choices.

The goal isn’t perfect tracking—it’s sufficient awareness to make informed financial decisions and catch problems early.

Saving and Investing for Beginners: Building Long-Term Wealth

Saving and investing are different activities serving different purposes. Understanding this distinction is crucial for building comprehensive financial security.

Saving vs. Investing

Saving means setting aside money in safe, liquid accounts for short-term goals and emergencies. Your principal is protected, you can access funds quickly, but growth is modest (currently 4-5% in high-yield savings accounts).

Investing means putting money into assets with growth potential—stocks, bonds, real estate, businesses. Your money can grow substantially over time but involves risk and short-term volatility. Investments are for long-term goals (5+ years away).

The Saving Priority Order

Emergency fund in savings accounts (3-6 months of expenses)

Short-term goal savings (vacation fund, car replacement, home down payment)

High-interest savings accounts for all the above

Beginning Your Investment Journey

Once you have adequate emergency savings and have addressed high-interest debt, investing builds long-term wealth.

Start with Retirement Accounts:

401(k) through Employers: If your company offers 401(k) matching, contribute at least enough to capture the full match—it’s free money. A typical match might be 50% of your contribution up to 6% of salary. Not capturing this match is leaving significant compensation unclaimed.

IRAs (Individual Retirement Accounts): Traditional IRAs provide tax deductions now with taxes paid in retirement. Roth IRAs use after-tax money but grow tax-free forever. For most young people, Roth IRAs offer superior long-term benefits.

Contribution Targets: Aim to invest 10-15% of gross income for retirement. Can’t afford this initially? Start with 3-5% and increase by 1% annually or whenever you get raises.

Investment Basics for Beginners

Diversification is Protection: Don’t put all money in one investment. Spread across different asset types (stocks, bonds) and different companies/sectors. When one investment underperforms, others may compensate.

Index Funds Over Stock Picking: Picking individual stocks is essentially gambling—you’re betting you can predict the future better than millions of other investors. Index funds own tiny pieces of hundreds or thousands of companies, providing instant diversification and matching market returns. Over decades, this approach beats most professional investors.

Time Beats Timing: You cannot reliably predict market highs and lows. Instead of timing the market (impossible), spend time in the market. Long-term, consistent investing beats attempting to perfectly time entry and exit points.

Compound Growth is Magic: Small amounts invested young grow dramatically through decades of compound returns. Invest $200 monthly from age 25-65 at 8% average returns, and you’ll have roughly $700,000. Wait until 35 to start, and you’ll have only about $300,000—half as much despite contributing for 30 years instead of 40.

Starting When You’re Completely New

Robo-Advisors: Platforms like Betterment, Wealthfront, or your bank’s robo-advisor service ask questions about your goals and risk tolerance, then automatically build and manage a diversified portfolio. Perfect for beginners who want professional management without high fees.

Target-Date Funds: These “set it and forget it” funds automatically adjust from aggressive (more stocks) when you’re young to conservative (more bonds) as you approach retirement. Choose the fund closest to your expected retirement year.

Start Small but Start Now: Can’t invest much? Start anyway. Many platforms allow investing with no minimums. Investing $25 monthly teaches valuable lessons while building the habit. Increase contributions as income grows.

Keep Learning: Read beginner investment books, take free online courses, or consult with fee-only financial advisors. Never invest in anything you don’t understand.

The combination of consistent saving for near-term security and strategic investing for long-term growth creates comprehensive financial health. Both deserve attention in your financial plan.

How to Be Financially Responsible in Your 20s (And Beyond)

Your twenties set patterns that echo throughout life. Developing financial responsibility early creates exponential advantages.

Start Retirement Contributions Immediately

“I’m too young to worry about retirement” is perhaps the costliest mistake young adults make. In your twenties, time is your superpower. Money invested at 25 has four decades to compound before retirement—potentially doubling five or six times.

Starting retirement contributions in your twenties versus thirties can create hundreds of thousands of dollars difference despite similar total contributions. This happens because early contributions have so much longer to grow.

Build Credit Thoughtfully

Your credit score affects apartment rentals, car insurance rates, job opportunities, and loan terms for decades. Build it intelligently:

Get a starter credit card and pay the full balance monthly

Keep credit utilization under 30% of limits

Pay all bills on time—set up automatic payments

Check your credit report annually for errors

Don’t close old credit cards (length of history matters)

Live Below Your Means

The gap between what you earn and what you spend determines financial success more than income alone. Someone earning $50,000 who spends $40,000 has more financial power than someone earning $100,000 who spends $105,000.

Resist lifestyle inflation. When you get raises or promotions, bank the increase rather than immediately upgrading your apartment, car, or wardrobe. Living like you make 80% of your actual income creates margin for savings, investing, and handling life’s surprises.

Create Multiple Income Streams

Relying on one income source is risky. Explore side hustles aligned with your skills—freelancing, consulting, online businesses, or gig economy work. Additional income accelerates debt payoff and savings while building skills and reducing dependence on a single employer.

Invest in Yourself

Education, skills, health, and relationships are investments that compound forever. Take courses that increase earning potential. Network intentionally. Maintain physical and mental health—medical bills from neglected health devastate finances.

Your human capital—your ability to earn income—is your most valuable asset in your twenties. Nurture it aggressively.

Avoid Major Financial Mistakes

Certain decisions in your twenties create decade-long consequences:

Don’t accumulate consumer debt for lifestyle inflation

Don’t cosign loans for friends or romantic partners

Don’t skip insurance to save money

Don’t withdraw retirement funds early (penalties and lost growth are devastating)

Don’t make financial decisions to impress others

The freedom to make mistakes is greatest in your twenties because you have time to recover—but why waste years recovering from avoidable errors?

Practice Delayed Gratification

Your twenties present constant temptation—friends’ trips, expensive hobbies, lifestyle upgrades. Learning to delay gratification distinguishes those who build wealth from those who perpetually struggle.

You can have almost anything you want—just not everything simultaneously right now. Prioritize ruthlessly, achieve goals sequentially, and discover that delayed pleasures are often sweeter than instant gratification.

Financial responsibility isn’t about sacrifice—it’s about playing the long game while others sprint aimlessly.

Simple Personal Finance Tips That Make a Big Difference

Small changes compound into significant results. These simple personal finance tips require minimal effort but deliver maximum impact:

Automate Everything Possible

Set up automatic transfers to savings, automatic bill payments, automatic retirement contributions, and automatic debt payments above minimums. Automation removes decision fatigue and prevents forgotten payments.

Use Cash for Problem Categories

If certain spending categories consistently exceed budget—restaurants, shopping, entertainment—switch to cash-only. Physical money creates psychological friction that digital payments lack, naturally reducing overspending.

Implement a Spending Freeze

Choose one category monthly where you spend zero: no restaurants, no shopping, no entertainment purchases. Redirect the savings to financial goals while discovering free or low-cost alternatives.

Unsubscribe Relentlessly

Marketing emails trigger spending impulses. Unsubscribe from promotional emails and abandon shopping apps. You can’t buy what you don’t see.

Calculate Purchases in Work Hours

Before buying something, convert the cost to work hours. That $200 jacket represents 10+ hours of work after taxes. Worth it? Sometimes yes, often no. This mental shift reveals whether purchases align with your values.

Master the Grocery Store

Meal planning, shopping with lists, buying generic brands, and cooking at home are among the highest-return habits. Families easily save $300-500 monthly with improved grocery strategies.

Negotiate Everything

Call service providers annually to negotiate lower rates on internet, phone plans, insurance, and subscriptions. Companies often offer discounts to retain customers—you just need to ask.

Use the Library

Books, movies, music, magazines, online courses, audiobooks—libraries offer massive value absolutely free. Entertainment and education without cost.

Practice the One-In-One-Out Rule

When buying something new, remove something similar you already own. This prevents accumulation while maintaining intentional consumption habits.

Create a Found Money Plan

Decide in advance what you’ll do with windfalls before receiving them. Tax refunds, bonuses, gifts, rebates—these go to financial goals rather than lifestyle inflation. Decide the plan once rather than trusting willpower in the moment.

None of these tips alone transforms finances, but implementing five or six simultaneously creates remarkable momentum.

How to Start Budgeting with Low Income

“Budgeting is for people with money to manage. I’m broke!” This misconception prevents the very people who would benefit most from budgeting from using it.

The truth: budgeting matters more when income is limited. Every dollar must work harder, making intentional allocation critical.

Acknowledge the Reality

Low income creates genuine challenges. Budgeting won’t magically create money that doesn’t exist. However, it ensures every available dollar serves your priorities rather than disappearing into forgotten micro-purchases.

Start with the Four Walls

When money is extremely tight, prioritize these four absolute essentials first:

Food (basic groceries, not restaurants)

Shelter (rent/mortgage and utilities)

Transportation (to work)

Essential clothing and medicine

Everything else comes after these are covered. This prioritization ensures survival while you build toward stability.

Find Every Available Dollar

Cut to Essentials: Eliminate every non-essential expense temporarily—subscriptions, entertainment, dining out, convenience purchases. This isn’t forever, but financial emergencies require intense focus.

Increase Income: Even $10 or $20 weekly from recycling, online surveys, neighborhood services (pet-sitting, lawn care), or selling unused items helps. Small amounts matter significantly at low income levels.

Seek Assistance: Research available resources without shame—food banks, utility assistance programs, community resources, government benefits. These programs exist to help during difficult times.

Negotiate Bills: Explain your situation to service providers and creditors. Many offer hardship programs, payment plans, or temporary relief you’ll never receive unless you ask.

Use Zero-Based Budgeting

With limited income, zero-based budgeting ensures every dollar has a specific assignment. This prevents “it disappeared somewhere” syndrome that’s devastating when money is already scarce.

Build a Micro Emergency Fund

Even $25 or $50 saved provides more security than zero. This tiny buffer prevents $20 overdraft fees or payday loan desperation when small emergencies strike.

Focus on Progress, Not Perfection

Your budget won’t look like someone earning double or triple your income—that’s expected. Compare your situation to your own past, not others’ present. Any improvement is success worth celebrating.

Low income budgeting requires more creativity and discipline, but the skills you develop during this season become superpowers when income eventually increases.

Step-by-Step Money Management Plan

Feeling overwhelmed by everything you’ve learned? This step-by-step money management plan provides a clear roadmap.

Month 1: Assess and Plan

Week 1: Gather all financial documents and calculate your complete financial picture—income, expenses, debts, assets.

Week 2: Track every purchase for two weeks to understand actual spending patterns.

Week 3: Create your first budget using your preferred method (50/30/20, zero-based, or envelope system).

Week 4: Set your initial SMART financial goals—starter emergency fund, specific debt payoff, or savings target.

Month 2-3: Build Your Foundation

Establish automatic savings: Set up automatic transfers to savings every payday for your starter emergency fund ($1,000-$2,000).

Implement your budget: Live on your budget, tracking daily and reviewing weekly. Adjust as you learn your true spending patterns.

Cut unnecessary expenses: Identify and eliminate spending that doesn’t align with your values or goals.

Open a high-yield savings account: Move your emergency fund to an account earning actual interest.

Month 4-6: Develop Habits

Complete your starter emergency fund: Hit that $1,000-$2,000 target through consistent contributions.

Start debt payoff: If you have high-interest debt, begin attacking it using snowball or avalanche method.

Review and refine your budget: By now you understand your patterns. Optimize category allocations.

Begin financial education: Read one personal finance book or take one online course on money management.

Month 7-12: Build Momentum

Continue debt elimination: If applicable, aggressively pay down consumer debt while maintaining minimum emergency fund.

Increase savings rate: Look for ways to save additional 1-2% of income.

Start retirement contributions: If you haven’t already, begin contributing to 401(k) or IRA, even if just 3-5% of income.

Evaluate progress: Compare your current financial situation to where you started. Celebrate improvements and identify areas needing attention.

Year 2: Accelerate

Build full emergency fund: Once consumer debt is eliminated, aggressively build 3-6 months of expenses in emergency savings.

Increase retirement contributions: Target 10-15% of gross income going to retirement accounts.

Pursue medium-term goals: Start saving for larger goals like home down payment or vehicle replacement.

Automate more: As habits solidify, automate additional aspects of your financial system.

Year 3+: Optimize and Grow

Maximize retirement contributions: Work toward maxing out 401(k) ($23,000 limit) and IRA ($7,000 limit) annually.

Diversify investments: Explore taxable investment accounts once retirement accounts are funded.

Increase income: Leverage skills and experience gained to negotiate raises, change jobs for better pay, or expand side hustles.

Consider additional goals: With strong foundation established, pursue goals like paying off mortgage early, funding children’s education, or achieving financial independence.

This timeline isn’t rigid—your pace depends on income, expenses, and existing debt. The key is consistent progress, not perfect execution.

Frequently Asked Questions About Personal Finance for Beginners

What is the 50/30/20 budget rule?

The 50/30/20 rule is a simple budgeting framework that allocates your after-tax income into three categories: 50% for needs (housing, utilities, groceries, transportation, insurance), 30% for wants (entertainment, dining out, hobbies, subscriptions), and 20% for savings and debt repayment beyond minimums. This provides clear guidelines without requiring detailed category tracking, making it ideal for beginners who want structure without complexity.

How much money should I have in my emergency fund?

Start with a $1,000-$2,000 starter emergency fund if you have consumer debt. Once debt-free, build a full emergency fund covering 3-6 months of essential living expenses. Choose 3 months if you have stable employment and dual income, or 6+ months if you’re self-employed, single income household, or have dependents. Calculate your actual monthly expenses for necessities only, then multiply by your target number of months.

Should I pay off debt or save money first?

Build a small starter emergency fund of $1,000-$2,000 first to prevent new debt during emergencies. Then aggressively attack high-interest debt like credit cards while maintaining that starter fund. Once consumer debt is eliminated, build your full 3-6 month emergency fund. This balanced approach provides basic protection while making progress on debt, preventing the cycle of paying off debt only to accumulate more when unexpected expenses hit.

How do I start investing with little money?

Begin with employer 401(k) plans if available, contributing at least enough to capture any company match. Open a Roth IRA through low-cost providers that don’t require minimums, such as robo-advisors or index fund companies. Start with whatever amount you can consistently afford, even $25-50 monthly. Choose target-date funds or total market index funds that provide instant diversification. As income grows, gradually increase contributions by 1% annually or whenever you receive raises.

What’s the difference between a Roth IRA and Traditional IRA?

Traditional IRAs provide tax deductions on contributions now, reducing your current taxable income, but you’ll pay taxes on withdrawals in retirement. Roth IRAs use after-tax money with no immediate deduction, but all growth and withdrawals in retirement are completely tax-free. For most young people in lower tax brackets, Roth IRAs offer better long-term value since you pay taxes at today’s likely lower rate and enjoy decades of tax-free growth.

How can I stop living paycheck to paycheck?

Start by tracking every expense for one month to identify where money actually goes. Create a realistic budget that prioritizes necessities first, then savings, then wants. Build even a small buffer of $500-1,000 through cutting unnecessary expenses, selling unused items, or earning extra through side work. Live on last month’s income if possible by getting one month ahead. Automate savings transfers every payday before you’re tempted to spend. Address underlying causes like lifestyle inflation or emotional spending through conscious reflection on your values and priorities.

Is it better to pay off debt or invest?

Generally, pay off high-interest debt (credit cards, payday loans, anything above 7-8% interest) before investing significantly beyond employer 401(k) matches. The guaranteed return from eliminating 18-24% interest debt beats uncertain investment returns. For moderate interest debt like student or car loans at 4-6%, you might split focus—making regular payments while also investing for retirement. For low-interest debt like mortgages at 3-4%, investing often makes more mathematical sense while making regular payments.

How do I create a budget when my income varies?

Use your lowest month’s income from the past 6-12 months as your baseline budget amount. This conservative approach ensures you can always cover necessities. When you earn above that baseline, immediately allocate the extra to specific goals—emergency fund, debt, or savings—rather than letting it disappear. Prioritize expenses in order of importance: start with the four walls (food, shelter, utilities, transportation), then other necessities, then savings, then wants. Build a larger emergency fund to compensate for income uncertainty.

Conclusion: Your Personal Finance Journey Starts Today

Personal finance for beginners isn’t about becoming a financial expert overnight. It’s about taking control of your money one decision at a time, building habits that compound into life-changing results.

You now understand the fundamentals: what personal finance encompasses, how to create a working budget, the importance of emergency funds, strategies for managing debt, and approaches to saving and investing. More importantly, you have a clear roadmap for implementation.

The perfect time to start was ten years ago. The second-best time is right now.

Begin with just one action today. Maybe it’s opening that high-yield savings account. Perhaps it’s tracking your spending for one week. Or possibly it’s having an honest conversation with your partner about financial goals. Whatever resonates most, do that one thing.

Tomorrow, do one more thing. Next week, another. Small consistent actions create momentum that transforms into unstoppable progress.

Your financial situation doesn’t define your worth, and past mistakes don’t determine your future. Every expert was once a beginner. Every financially stable person once struggled with these same challenges you’re facing.

The difference between financial stress and financial peace isn’t your income level—it’s your willingness to learn, apply proven principles consistently, and give yourself grace during the learning process.

Your journey to financial confidence and security starts with a single step. Take it today.

We are not promoting any of these websites. These links are shared only for educational purposes to help readers access reliable financial information.

My friend Jake dropped $45 on a single dinner last week. Not because he’s rich—he makes about $52K as a graphic designer. But here’s the kicker: he’s also got $18,000 sitting in his savings account and contributes 15% to his 401k every month.

Ten years ago, this would’ve been financial blasphemy. “Skip the avocado toast!” the experts screamed. “Make coffee at home!” But Jake represents something bigger happening right now—people are completely rewriting the rulebook on money, and honestly? A lot of it makes way more sense than the old advice ever did.

I’ve been tracking these shifts for months, talking to friends, reading studies, and watching how people actually spend and save (not how they say they do). What I found surprised me. We’re not just tweaking the old system—we’re building an entirely new one from scratch.

1. Revenge Saving Is the New Emergency Fund

Preparing for the unexpected by saving cash in an emergency fund.

Remember when financial advisors told you to save three months of expenses “just in case”? Well, meet Emma. She’s 26, works in HR, and has fourteen months of living expenses saved up. Not because she’s planning anything specific, but because watching her older sister get laid off during COVID and scramble for rent money scared the hell out of her.

She calls it her “never again” fund. I’ve heard other people call it revenge saving—basically hoarding cash like you’re preparing for financial war.

Emma isn’t alone. I know at least six people who’ve got 12+ months saved, way beyond what any traditional advice suggests. They’re not doing it for early retirement or a house down payment. They’re doing it because uncertainty feels like the only certainty right now.

Here’s what’s wild: most of these folks aren’t stressed about their money anymore. That massive cash pile bought them something you can’t put a price on—mental peace.

The smart move: Figure out your own “sleep well at night” number. Maybe it’s six months, maybe it’s two years. There’s no wrong answer if it keeps you from lying awake worrying about bills.

The trap: Don’t let all that cash just sit there losing value to inflation. Once you hit your comfort zone, start moving the extra into investments. Your future self will thank you.

2. The “Fun Money” Revolution

Here’s something that would make Dave Ramsey’s head explode: people are budgeting for completely frivolous stuff and feeling zero guilt about it.